Keeping global warming to less than 2C above pre-industrial temperatures is "crucial" for limiting damage to the Antarctic Peninsula's unique ecosystems, according to a new study.

The paper, published in Frontiers in Environmental Science, reviews the latest literature on the impacts of warming on Antarctica's most biodiverse region.

The Antarctic Peninsula is home to many types of penguins, whales and seals, as well as the continent's only two flowering plant species.

The study also analyses previously published data and model output to create a fuller picture of the potential futures facing the peninsula under different levels of global warming.

Under a low-emissions scenario that keeps global temperature rise to less than 2C, the Antarctic Peninsula will still face 2.28C of warming by the end of the century, the study says, while higher-emissions futures could push the region's warming above 5C.

Limiting warming to 2C would avoid the more dramatic impacts associated with higher emissions, such as ice-shelf collapse, increasingly frequent extreme weather events and extinction of some of the peninsula's native species, according to the paper.

However, warming of 4C would result in "dramatic and irreversible" damages, it adds.

Importantly, the paper shows that the outlook for the peninsula is "dependent on the choices we make now and in the near future", a researcher not involved in the study tells Carbon Brief.

'Alternative futures'The Antarctic Peninsula juts northwards from West Antarctica, stretching towards the tip of South America.

The region is made up of the main peninsula, which spans around 232,000 square kilometres (km2) and a series of islands and archipelagos that cover another 80,000km2. The mainland peninsula is nearly entirely covered in ice, while its islands - many of which are further north - are around 92% covered.

Taken as a whole, the Antarctic Peninsula is the most biodiverse region of the icy continent, and a "beautiful, pristine environment", says Prof Bethan Davies, a glaciologist at Newcastle University, who led the new work.

It hosts many species of penguins and whales, as well as apex predators, such as orcas and leopard seals. Each spring, more than 100m birds nest there to rear their young. It is also home to hundreds of species of moss and lichens, along with the only two flowering plant species on the continent.

The peninsula is also the part of Antarctica that is undergoing the most significant changes due to climate change, according to the Intergovernmental Panel on Climate Change's (IPCC's) sixth assessment report.

In 2019, a group of researchers published a study on the fate of the Antarctic Peninsula at 1.5C of global warming above pre-industrial temperatures. However, it has since "become apparent" that keeping warming below this limit is no longer in reach, Davies says.

The team selected three warming scenarios for their study:

- a low-emissions scenario, SSP1-2.6

- a high-emissions scenario characterised by growing nationalism, SSP3-7.0

- a very-high-emissions scenario, SSP5-8.5

SSP1-2.6 represents the "new goal" of keeping warming less than 2C, Davies says.

SSP3-7.0 and SSP5-8.5 represent "alternative futures" - with the former being one that "felt quite relevant" to the current state of the world and the latter being "useful to consider as a high end", she adds.

For each potential future, the researchers conducted a literature review to assess the changes to different parts of the peninsula's physical and biological systems. To fill gaps in the published literature, the team also reanalysed existing datasets and results from the Coupled Model Intercomparison Project 6 (CMIP6) group of models developed for the IPCC's latest assessment cycle.

Dr Sammie Buzzard, a glaciologist at the Centre for Polar Observation and Modelling, tells Carbon Brief:

"By choosing three different emissions scenarios, they've shown just how much variability there is in the possible future of the Antarctica Peninsula that is dependent on the choices we make now and in the near future."

Buzzard, who was not involved in the new study, adds that it "highlights the consequences of this [change] for the glaciers, sea ice and unique wildlife habitats in this region".

Physical changesThe Antarctic Peninsula is already experiencing climate change, with one record showing sustained warming over nearly a century. The peninsula is also warming more rapidly than the global average.

For the new study, Davies and her team assess the changes in temperature for the decade 2090-99 across 19 CMIP6 models.

They find that under the low-emissions scenario, the Antarctic Peninsula is projected to warm by 2.28C compared to pre-industrial temperatures, or about 0.55C above its current level of warming. Under the high- and very-high-emissions scenarios, the peninsula will reach temperatures of 5.22C and 6.10C above pre-industrial levels, respectively.

They also analyse output from 12 sea ice models.

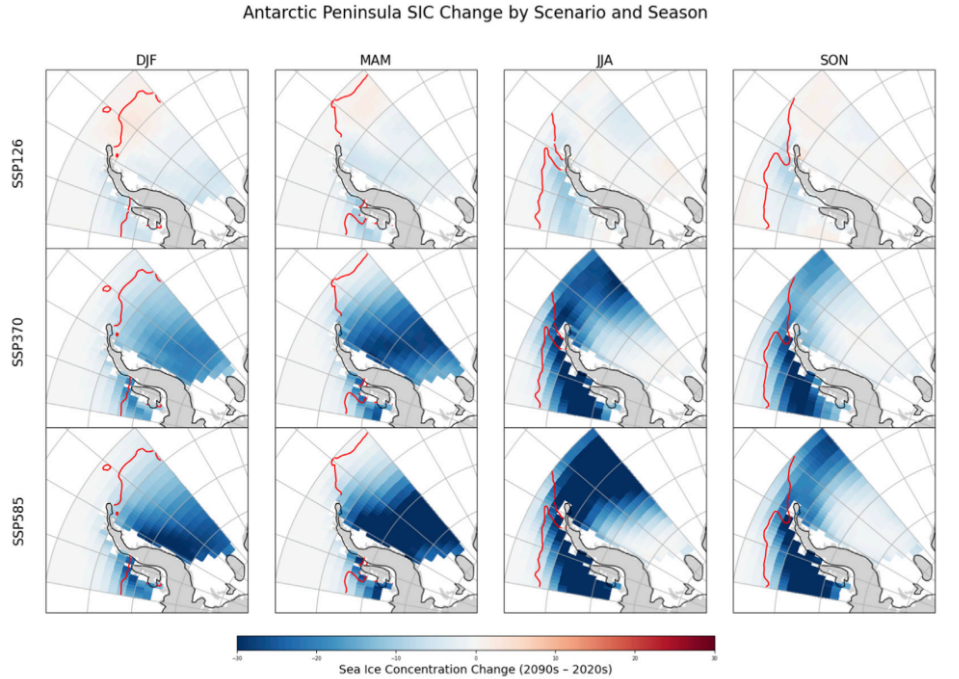

In each scenario, they find that the western side of the Antarctic Peninsula experiences the largest declines in sea ice concentration during the winter months of June, July and August. For the southern hemisphere's summertime, it is the eastern side of the peninsula that shows the largest decreases.

The maps below show the projected change in sea-ice concentration around the Antarctic Peninsula for each season (left to right) under low (top), high (middle) and very high (bottom) emissions. Decreasing concentrations are shown in blue and increasing concentrations are shown in red.

Changes in the concentration of sea ice around the Antarctic Peninsula in the 2090s, as compared to the 2020s. Decreases (increases) in sea ice concentration are shown in blue (red). The rows show the different future pathways (top to bottom): SSP1-2.6, SSP3-7.0 and SSP5-8.5. The columns show three-month chunks of the year (left to right): December, January and February; March, April and May; June, July and August; and September, October and November. Source: Davies et al. (2026)

Changes in the concentration of sea ice around the Antarctic Peninsula in the 2090s, as compared to the 2020s. Decreases (increases) in sea ice concentration are shown in blue (red). The rows show the different future pathways (top to bottom): SSP1-2.6, SSP3-7.0 and SSP5-8.5. The columns show three-month chunks of the year (left to right): December, January and February; March, April and May; June, July and August; and September, October and November. Source: Davies et al. (2026)

The paper gives a "great overview of the current literature on the Antarctic Peninsula, examining multiple aspects of the region holistically", Dr Tri Datta, a climate scientist at the Delft University of Technology, tells Carbon Brief.

However, Datta - who was not involved in the study - notes that the coarse resolution of CMIP6 models means that the "most vulnerable regions are too poorly represented to capture important feedbacks", such as the forming of meltwater ponds on the tops of glaciers, which warm much more than the icy surface around them.

Ecosystem impactsThe study also looks at potential futures for the Antarctic Peninsula's marine and terrestrial ecosystems - albeit, much more briefly than it examines the physical changes.

This is because modelling ecosystem change is very difficult, Davies explains:

"If you're going to model an ecosystem, you have to model the climate and the ocean and the ice and how that changes. Exactly how that ecosystem responds to those changes is still beyond most of our Earth system models."

Still, by looking at trends in the Antarctic over the past several decades, as well as changes that have occurred in other high-latitude regions, the researchers piece together some of the potential impacts of warming.

They conclude that under SSP1, the changes experienced by ecosystems are "uncertain", but will "likely" be similar to present day - with some terrestrial species, such as its flowering plants, even benefitting from increased habitat area and water availability.

Flowering plants on rock crevices in Antarctica. Credit: Colin Harris / era-images / Alamy Stock Photo

Flowering plants on rock crevices in Antarctica. Credit: Colin Harris / era-images / Alamy Stock Photo

However, under higher-emissions scenarios, species will become "increasingly likely" to experience warmer temperatures than they are suited for.

Other changes that may occur in the very-high-emissions scenario are closely linked to the projected reductions in sea ice. These include the increased spread of invasive alien species, reduced ranges for krill and the displacement of animals unable to tolerate the warmer temperatures by those more able to adapt.

Prof Scott Doney, an oceanographer and biogeochemist at the University of Virginia, notes that some of these changes are already happening. Doney, who was not involved in the study, is part of an ongoing research programme on the Antarctic Peninsula known as the Palmer Long-Term Ecological Research project.

He tells Carbon Brief that Adélie penguins, which are a polar species, have "seen a massive drop in their breeding population" at their research sites. Meanwhile, gentoo penguins - whose range extends into the subpolar regions - "have been quite opportunistic" in colonising those breeding sites.

'Changes here first'Antarctica is home to 50 year-round research stations and dozens of summer-only ones, operated by more than 30 countries.

Around a dozen year-round stations are found on the peninsula and its islands, including the oldest permanent settlement in Antarctica - Argentina's Base Orcadas, established in 1903 by the Scottish national Antarctic expedition.

The continent is home to commercially important fisheries - particularly krill, which also play a critical role in the Antarctic marine food chain.

Increasingly, the Antarctic Peninsula is also a tourist destination.

Climate change poses a threat to all of these activities, Davies says.

For example, much of the research infrastructure on the Antarctic Peninsula was "built to assume dry, snowy conditions", she says. Rain can "cause quite a lot of difficulty", she adds.

(In an article published last year, Carbon Brief looked at the causes of rain in sub-zero temperatures in West Antarctica.)

Decreased sea ice cover can impact krill populations. It can also lead to increased ship traffic, as more of the continent becomes accessible throughout more of the year.

Furthermore, Davies says, the changes occurring on the peninsula will reverberate across Antarctica and around the world. She tells Carbon Brief:

"We'll see changes here first and those changes will continue to be felt in West Antarctica and continent-wide…What happens in Antarctica doesn't stay in Antarctica."

Antarctic sea ice winter peak in 2025 is third smallest on record

Antarctic

|01.10.25

Guest post: How atmospheric rivers are bringing rain to West Antarctica

Antarctic

|11.02.25

Antarctic sea ice maximum in 2024 is 'second lowest' on record

Antarctic

|04.10.24

Antarctic sea ice 'behaving strangely' as Arctic reaches 'below-average' winter peak

Antarctic

|26.03.24

jQuery(document).ready(function() { jQuery('.block-related-articles-slider-block_7658bad35ade9644b59c4fe06909d66a .mh').matchHeight({ byRow: false }); });The post Limiting warming to 2C is 'crucial' to protect pristine Antarctic Peninsula appeared first on Carbon Brief.

Welcome to Carbon Brief's China Briefing.

China Briefing handpicks and explains the most important climate and energy stories from China over the past fortnight. Subscribe for free here.

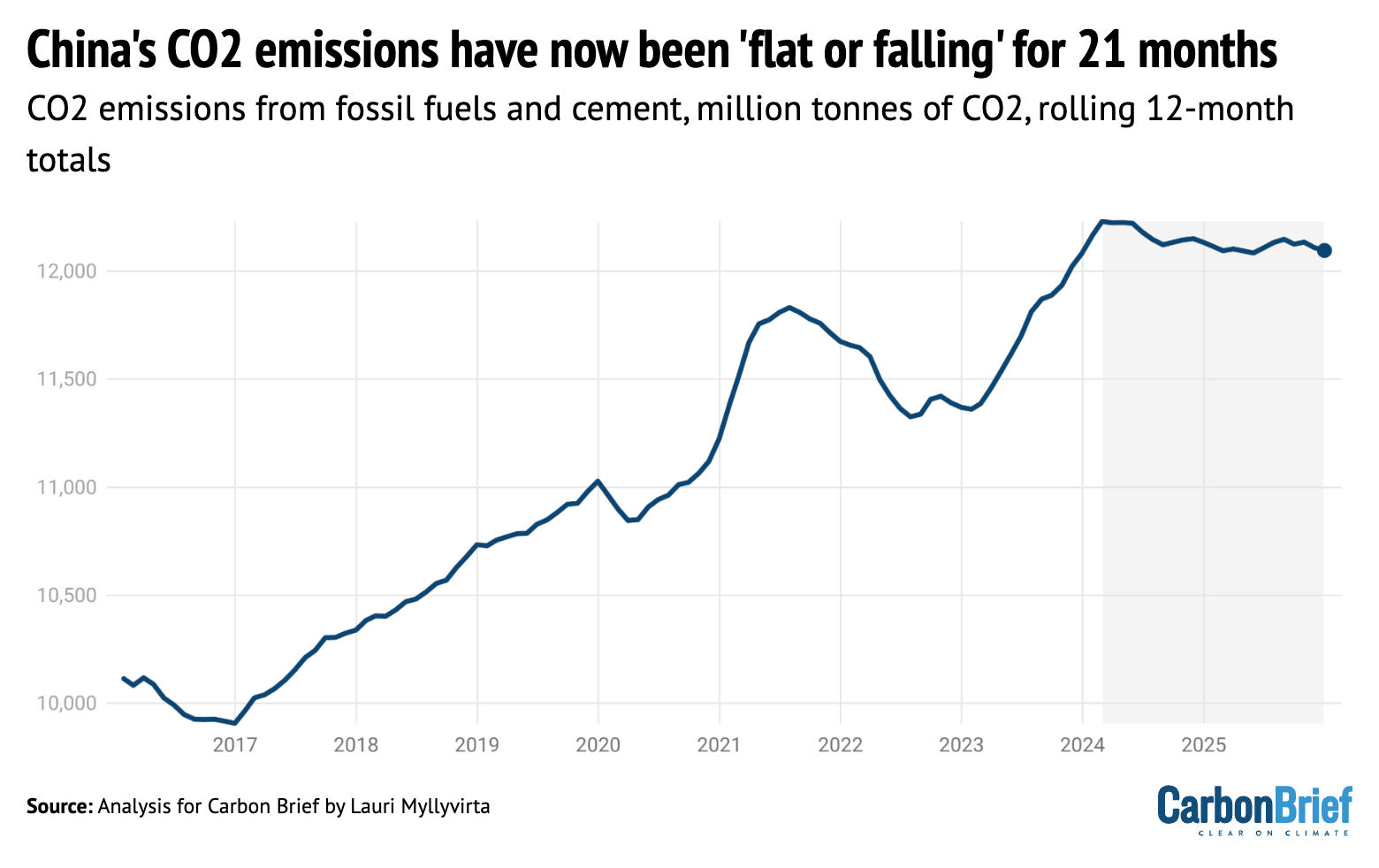

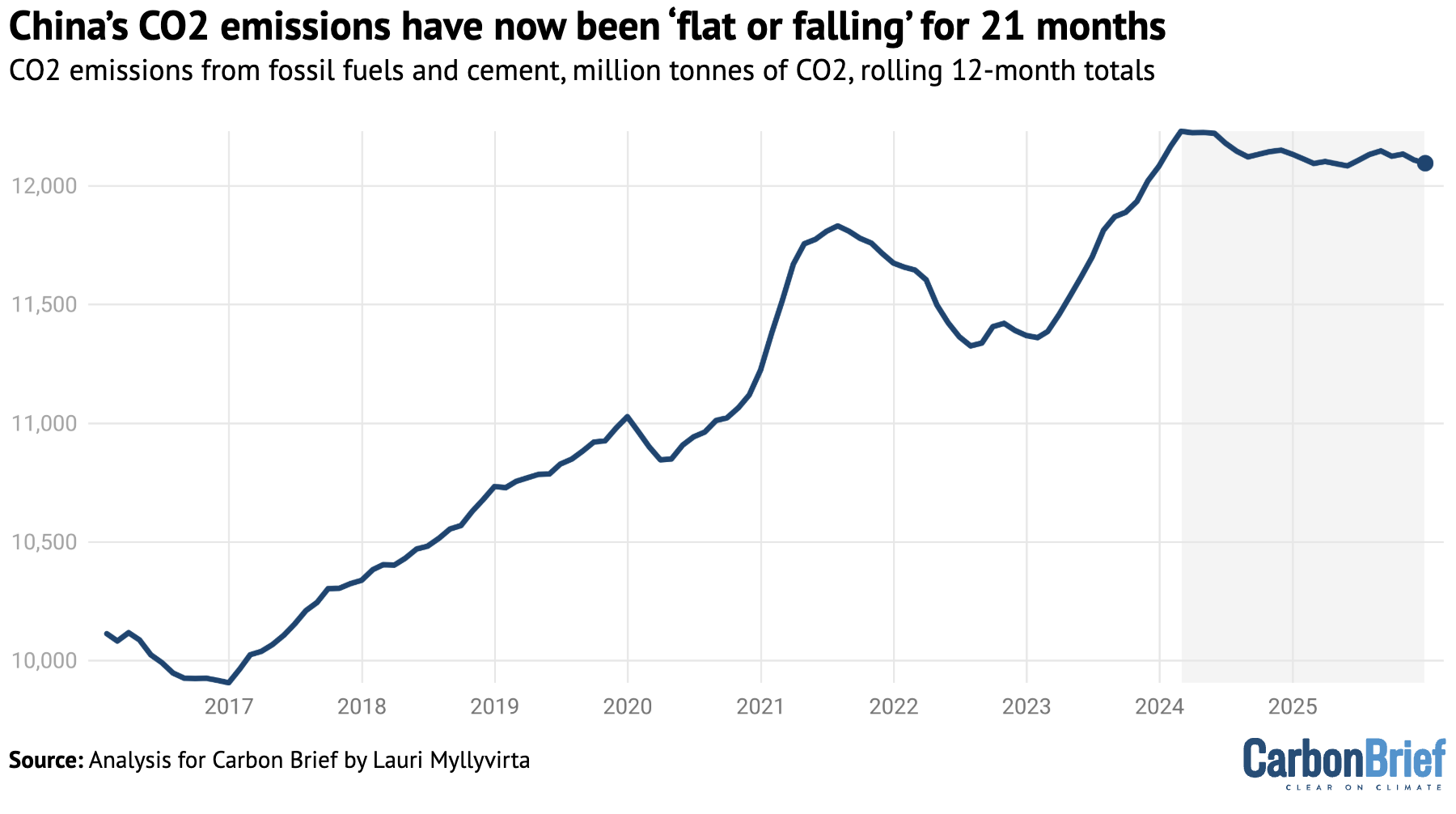

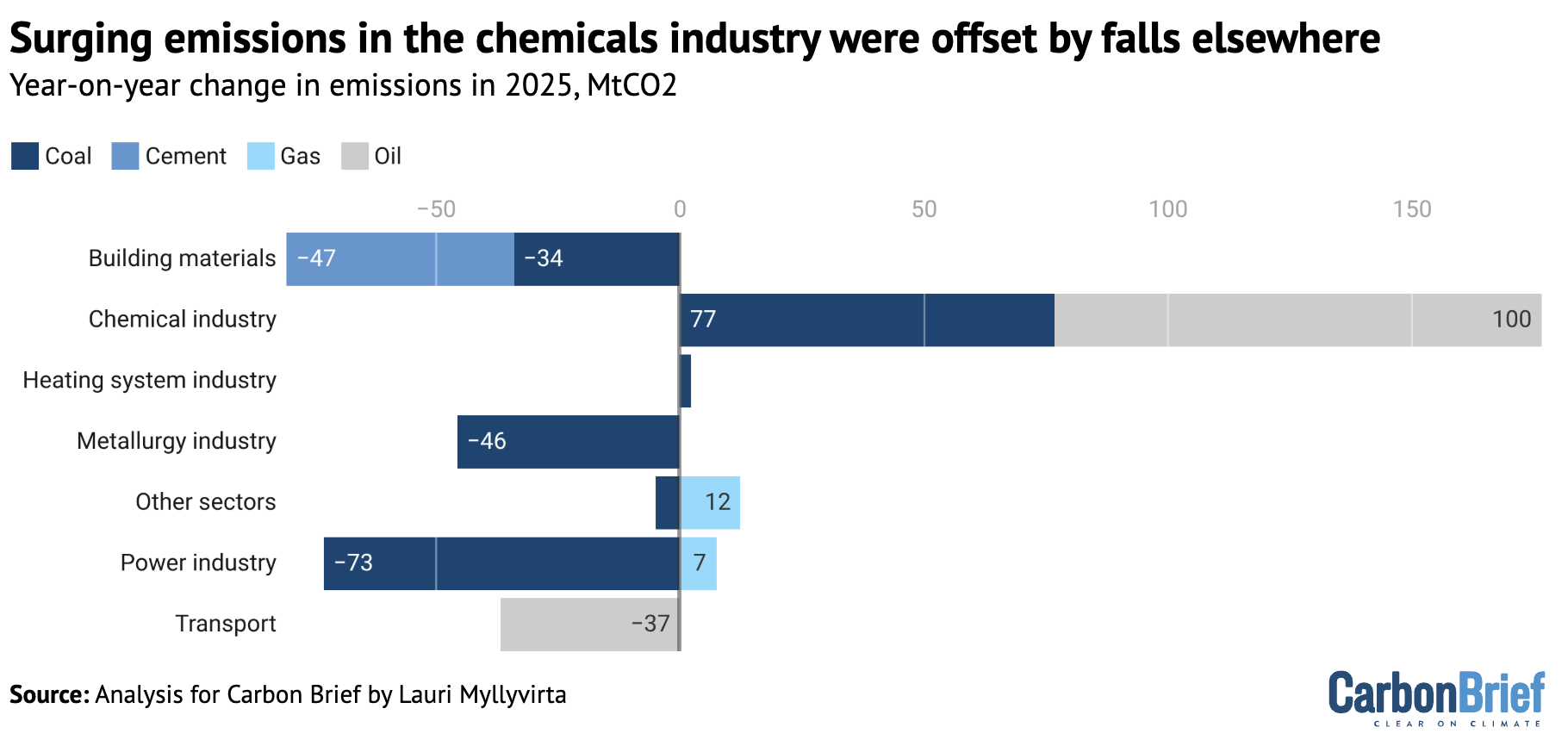

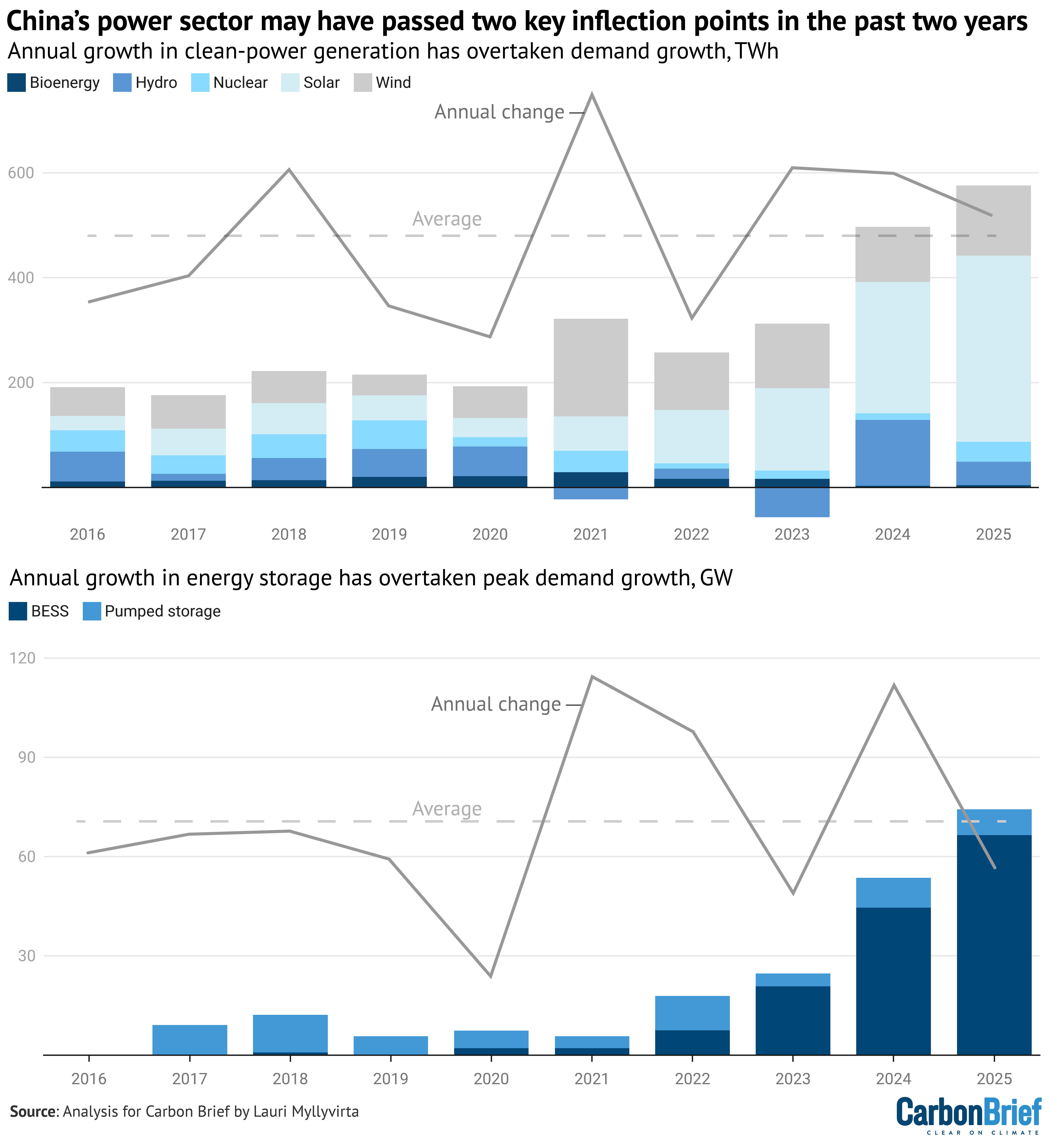

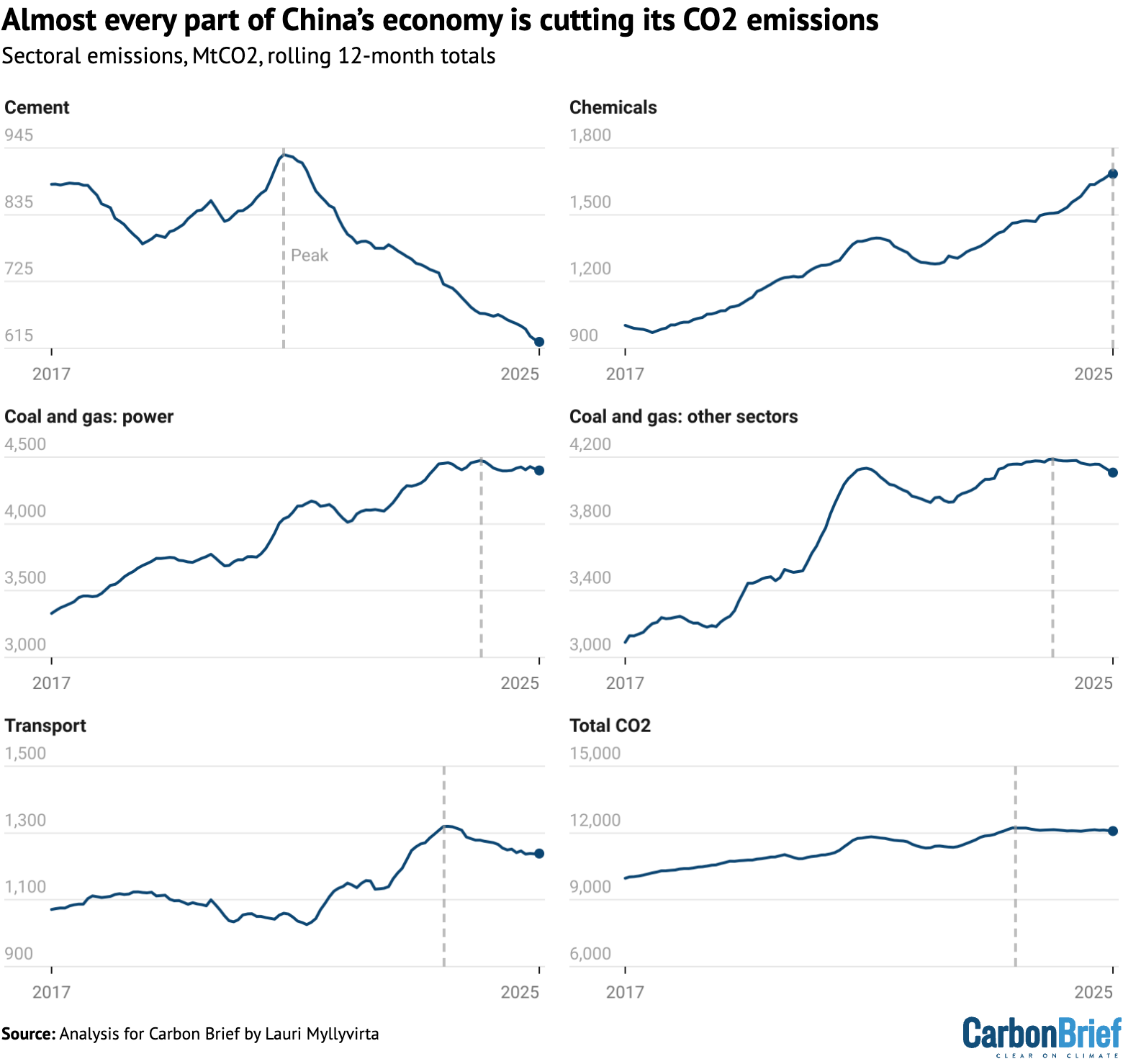

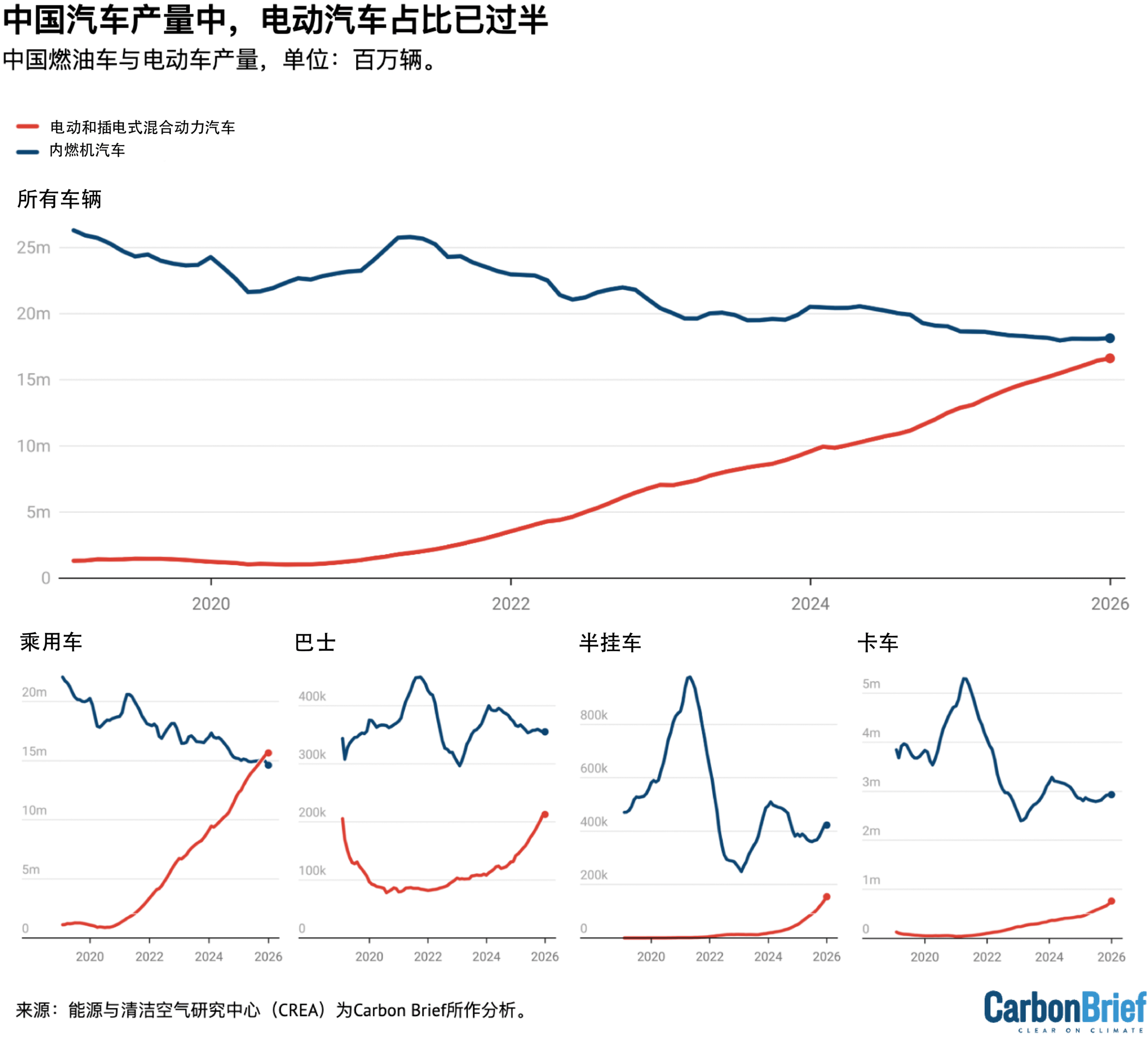

Key developments Carbon emissions on the decline'FLAT OR FALLING': China's carbon dioxide (CO2) emissions have been either "flat or falling" for almost two years, reported Agence France-Presse in coverage of new analysis for Carbon Brief by the Centre for Research on Energy and Clean Air (CREA). This marks the "first time" annual emissions may have fallen at a "time when energy demand was rising", it added. Emissions fell 0.3% during the year, driven by a fall in emissions "across nearly all major sectors", said Bloomberg - including the power sector. It said the chemicals sector was an exception, where emissions saw a "large jump from a surge of new plants using coal and oil" as feedstocks. The analysis has been covered around the world by outlets ranging from the New York Times, Bloomberg and BBC News through to Der Spiegel, CGTN and the Guardian.

TOP TASKS: President Xi Jinping listed "persisting in following the 'dual-carbon' goals" as one of eight "key" elements of economic work in 2026, according to a December speech just published in Qiushi, the Chinese Communist party's leading journal for political theory. This included "deeply advancing" carbon reduction in key industries and "steadily promoting a peak in consumption of coal and oil", according to the transcript. The National Energy Administration (NEA) also outlined a number of priority tasks for the department, including resolving "grid integration challenges" to encourage greater use of renewable energy and "boosting investment" in energy resources, said energy news outlet International Energy Net.

上微信关注《碳简报》

ETS EXPANSION: Meanwhile, the government has asked "heavy polluters" in several sectors not yet covered in China's emissions trading scheme (ETS) to report their emissions for 2025, reported Bloomberg, in a "key step" for the further expansion of the carbon market. The affected industries are the "petrochemical, chemical, building materials (flat glass), nonferrous metals (copper smelting), paper and civil aviation industries", according to the original notice posted by the Ministry of Ecology and Environment (MEE), as well as steel and cement companies not yet covered by the ETS.

State Council issued 'unified' power market guidancePOWER TRADE: China will aim for "market-based transactions" to account for 70% of total electricity consumption by 2030, according to new policy guidance released by China's State Council and published by International Energy Net. The policy also called for greater "integration" of cross-regional trading and "fundamentally sound" market-based pricing mechanisms. On renewable power, the guidance urged officials to "expand the scale of green power consumption" and establish a "green certificate consumption system that combines mandatory and voluntary consumption", as well as encourage "implementation of inter-provincial renewable energy priority dispatch plans". It also calls for "roll[ing] out spot trade nationwide by 2027, up from just 4% of the total transactions today", reported Bloomberg.

CLEAN-POWER PUSH: An official at China's National Development and Reform Commission said in a Q&A published by BJX News that establishing a "unified" national power market is "crucial for constructing a new power system". A separate analysis by Beijing-based power services firm Lambda reposted on BJX News argues that China's unified power-market reforms - which have been "more than two decades" in the making - will allow for "widespread integration" of renewable energy, resolving the challenge of wind and solar "generating but being unable to transmit and integrate". Business news outlet Jiemian quoted Xiamen University professor Lin Boqiang saying that, while power-market reform may present clean-energy companies with "growing pains" in the short term, it will "force the industry to develop healthily" in the long term.

EU tariffs lifted on first firm's China-built EV imports'SOFTENED' STANCE: The Chinese government has "softened its stance" on electric vehicle (EV) manufacturers who seek to independently negotiate with the EU on prices for their exports to the bloc, said Reuters, after it previously "urged the bloc not to engage in separate talks with Chinese manufacturers". The move came as Volkswagen received an exemption from tariffs for one of its EVs that is made in China and imported to the EU, which it committed to sell above a specific price threshold, reported Bloomberg. It added that the company also pledged to follow an import quota and "invest in significant battery EV-related projects" in the EU.

Subscribe: China Briefing- .listing{background: #f4f4f4} .listing ul{list-style:none; margin:0} ol {background: #F4F4F4; padding: 0px;} .listing ul {background: #F4F4F4; padding: 0px;} .listing li{font-size:0px;}

Sign up to Carbon Brief's free "China Briefing" email newsletter. All you need to know about the latest developments relating to China and climate change. Sent to your inbox every Thursday.

'MADE IN EU' MELTDOWN: Meanwhile, EU policymakers attempted to agree legislation that may force EV manufacturers to ensure "70% of the components in their cars are made in the EU" if they wish to receive subsidies, reported the Financial Times. A draft of the plan was ultimately rejected by nine European Commission leaders and commission president Ursula von der Leyen, Borderlex managing editor Rob Francis wrote on Bluesky.

BRAZIL BACKTRACKS: Brazil has "scrapped" a tariff exemption for Chinese EV manufacturers that allowed cars assembled in Brazil with parts imported from China to be sold at much lower prices than similar vehicles made from parts imported from other countries, reported the Hong Kong-based South China Morning Post. Separately, Bloomberg reported on the surge of tariff-free Chinese EVs that has enabled Ethiopia to ban the import of combustion-engine cars.

PRICE-WAR BAN: The Chinese government has "banned carmakers from pricing vehicles below cost", reported Bloomberg, in an effort to clamp down on a "persistent price war" affecting the industry. China's car industry, "particularly in the EV segment", has seen "aggressive discounting, subsidies and bundled promotions" pushing down profitability for companies across the supply chain, said the state-run newspaper China Daily.

More China news- POWERFUL WIND: China has connected a 20-megawatt offshore wind turbine - the "world's most powerful" and "equivalent to a 58-story building" - to the grid, reported state news agency Xinhua.

- PROVINCIAL MOVES: Anhui has become the first Chinese province to release data on how much carbon different forms of power in the province emits per kilowatt-hour of power, according to power news outlet BJX News.

- RARE-EARTH RUNES: China may hold a "policy briefing" on export restrictions for rare earths and other critical minerals in March, according to Reuters.

- NO CHINA CREDITS: The US confirmed that clean-energy tax credits will not be available for companies that are "overly reliant on Chinese-made equipment", said Reuters.

Carbon Brief spoke with Ma Jun, one of China's most well-known environmentalists, about how open data can keep pressure on industry to decarbonise and boost interest in climate change.

Ma is director of the Beijing-based Institute of Public and Environmental Affairs (IPE), an organisation most well known for developing the Blue Map, China's first public database for environment data.

Speaking to Carbon Brief during the first week of COP30 in Brazil last November, the discussion covered the importance of open data, key challenges for decarbonising industry, China's climate commitments for 2035, cooperation with the EU and more.

Below are highlights from the conversation. The full interview can be found on the Carbon Brief website.

Open data is helping strengthen climate policy- On how data transparency prevents environmental pollution in China: "From that moment [when the general public began flagging environmental violations on social media in 2014], it was no longer easy for mayors or [party] secretaries to try to interfere with the enforcement, because it's being made so transparent, so public."

- On encouraging the Chinese government to publish data: "The ministry felt that they had the backing from the people, basically, which helped them to gain confidence that data can be helpful and can be used in a responsible way."

- On China's new corporate disclosure rules: "We're talking about what's probably the largest scale of corporate measuring and disclosure now happening [anywhere in the world]."

- On the need for better emissions data: "It will be impossible to get started without proper, more comprehensive measuring and disclosure, and without having more credible data available."

- On the economics of coal: "There's no business interest for the coal sector to carry on, because increasingly the market will trend towards using renewables, because it's getting cheaper and cheaper".

- On paying for low-carbon products: "When we engage with them and ask why they didn't expand production, they say that producing these items will have a 'green premium', but no one wants to pay for that. Their users only want to buy tiny volumes for their sustainability reports."

- On public perceptions in China of climate change: "It's more abstract - [we're talking about] the end of the century or the polar bears. People don't feel that it's linked with their own individual behaviour or consumption choices."

- On criticism of China's climate pledge: "In the west, the cultural tendency is that if you want to show that you're serious, you need to set an ambitious target. Even if, at the end of the day, you fail, it doesn't mean that you're bad…But in China, the culture is that it is embarrassing if you set a target and you fail to fully honour that commitment."

- On global climate cooperation: "The starting point could be transparency - that could be one of the ways to help bridge the gap."

- On working in China as a climate NGO: "What we're doing is based on these principles of transparency, the right to know. It's based on the participation of the public. It's based on the rule of law. We cherish that and we still have the space to work [on these issues]."

- On the climate consensus in China: "The environment - including climate - is the area with the biggest consensus view in [China]. It could be a test run for having more multi-stakeholder governance in our country."

This interview was conducted by Anika Patel at COP30 in Belém on 13 November 2025.

Watch, read, listenGREEN ALUMINIUM: Lantau Group principal David Fishman wrote on LinkedIn about why China's aluminium smelters are seeking greater access to low-carbon power, following heated debate over a Financial Times article.

STRONGER THAN EVER: Isabel Hilton, chair of the Great Britain-China Centre, spoke on the Living on Earth podcast about China's renewables push and exports of clean-energy technologies.

CUTTING CORNERS?: Business news outlet Caixin examined how a surge in turbine defects at one wind farm could be due to "aggressive cost-cutting and rapid installation waves".

POLES APART: BBC News' Global News Podcast examined the drivers behind China's flatlining emissions, as revealed by Carbon Brief.

600

In gigawatts, China's total capacity of coal plants that are "flexible" and - in theory - better able to balance the variability of renewables, according to a new report by the thinktank Ember.

New science

- China will see a 41% decline in in coal-mining jobs over the next decade under current climate policies | Environmental Research Letters

- During 2000-20, China's per-person emissions of CO2 increased from 106kg to 539kg in urban households and from 35kg to 202kg in rural households, indicating that the inequality between urban and rural households is shrinking | Scientific Reports

China Briefing is written by Anika Patel and edited by Simon Evans. Please send tips and feedback to china@carbonbrief.org

China Briefing

|05.02.26

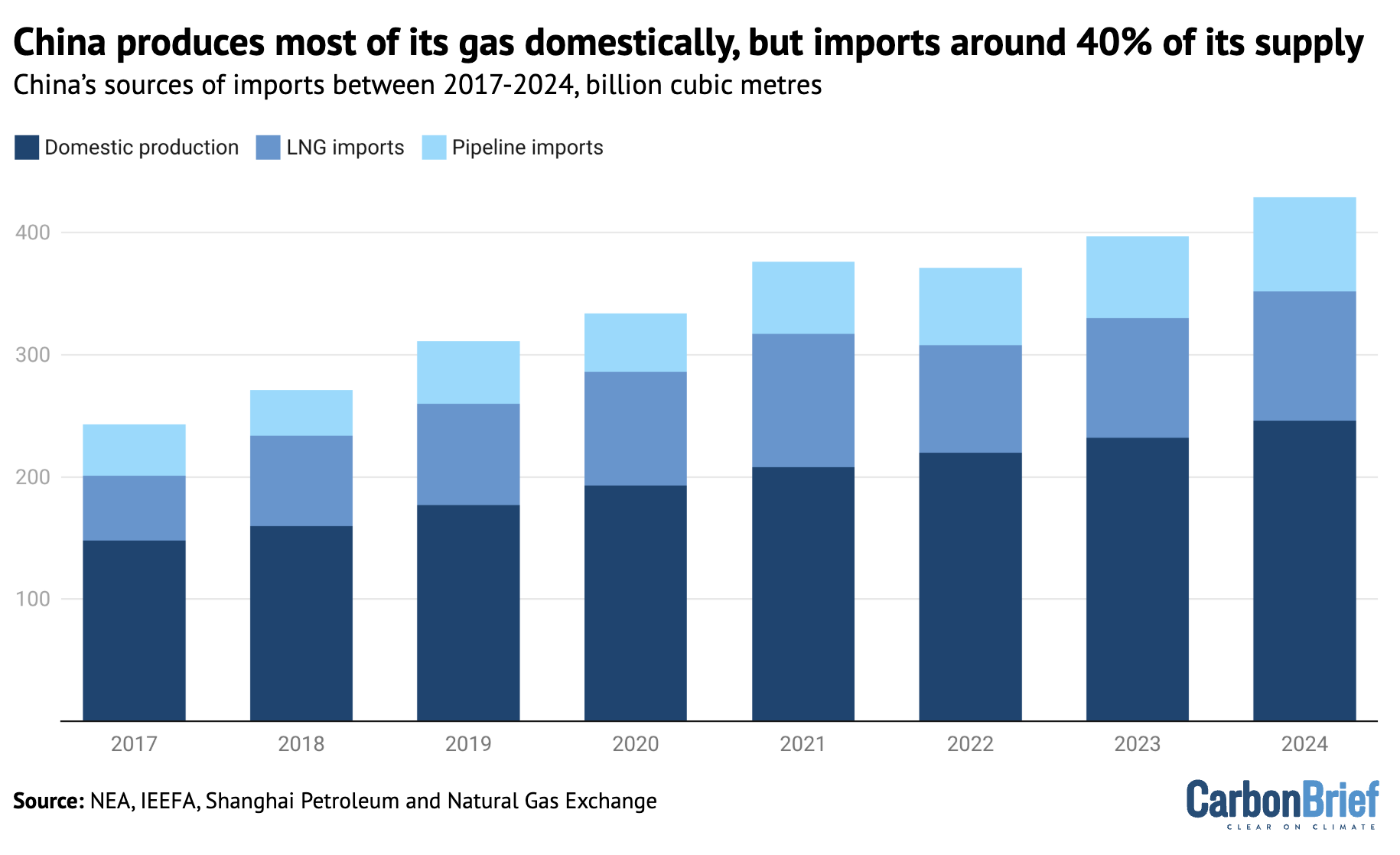

China Briefing 22 January 2026: 2026 priorities; EV agreement; How China uses gas

China Briefing

|22.01.26

China Briefing

|11.12.25

China Briefing 27 November 2025: COP30 wraps; Climate and critical minerals at G20; Coal use up

China Briefing

|27.11.25

jQuery(document).ready(function() { jQuery('.block-related-articles-slider-block_e1a2c53f1cd96ae1fbfe82bcf255083b .mh').matchHeight({ byRow: false }); });The post China Briefing 19 February 2026: CO2 emissions 'flat or falling' | First tariff lifted | Ma Jun on carbon data appeared first on Carbon Brief.

Open and transparent data can accelerate the decarbonisation of China's industries and boost public interest in climate change, says Ma Jun.

Ma - one of China's most recognisable environmental activists - says that early experiments with publishing real-time air quality data have paved the way for greater openness from the Chinese government towards publishing greenhouse gas emissions data.

However, he tells Carbon Brief in a wide-ranging interview, more needs to be done to encourage "multi-stakeholder" participation in climate efforts and to improve corporate emissions disclosure.

He also notes that China faces significant "challenges" in reducing emissions from "hard-to-abate" sectors, where companies struggle to find consumers willing to pay a "green premium" for low-carbon versions of their products.

Ma is the founder and director of the Institute of Public and Environmental Affairs (IPE), a Beijing-based NGO focused on environmental information disclosure and public participation.

The IPE is most well-known for developing the Blue Map, China's first public database for environment data.

Ma has been a long-term advocate for environmental protection in China.

Prior to founding the IPE, he covered environmental pollution as an investigative reporter at the Hong Kong-based South China Morning Post.

He also authored China's first book on the serious water pollution challenges facing the country.

Speaking to Carbon Brief during the first week of COP30 in Brazil last November, the discussion covered the importance of open data, key challenges for decarbonising industry, China's climate commitments for 2035, cooperation with the EU and more.

- On how data transparency prevents environmental pollution in China: "From that moment [that the general public began flagging environmental violations on social media], it was no longer easy for mayors or [party] secretaries to try to interfere with the enforcement, because it's being made so transparent, so public."

- On encouraging the Chinese government to publish data: "The ministry felt that they had the backing from the people, basically, which helped them to gain confidence that data can be helpful and can be used in a responsible way."

- On China's new corporate disclosure rules: "We're talking about what's probably the largest scale of corporate measuring and disclosure now happening [anywhere in the world]."

- On air-pollution policies creating a template for climate action: "It started from the pollution control side and now we want to see that happen on the climate side."

- On paying for low-carbon products: "When we engage with them and ask why they didn't expand production, they say that producing these items will have a 'green premium', but no one wants to pay for that. Their users only want to buy tiny volumes for their sustainability reports."

- On public perceptions of climate change: "It's more abstract - [we're talking about] the end of the century or the polar bears. People don't feel that it's linked with their own individual behaviour or consumption choices."

- On the need for better emissions data: "It will be impossible to get started without proper, more comprehensive measuring and disclosure, and without having more credible data available."

- On criticism of China's climate pledge: "In the west, the cultural tendency is that if you want to show that you're serious, you need to set an ambitious target. Even if, at the end of the day, you fail, it doesn't mean that you're bad…But in China, the culture is that it is embarrassing if you set a target and you fail to fully honour that commitment."

- On global climate cooperation: "The starting point could be transparency - that could be one of the ways to help bridge the gap."

- On the economics of coal: "There's no business interest for the coal sector to carry on, because increasingly the market will trend towards using renewables, because it's getting cheaper and cheaper".

- On working in China as a climate NGO: "What we're doing is based on these principles of transparency, the right to know. It's based on the participation of the public. It's based on the rule of law. We cherish that and we still have the space to work [on these issues]."

- On the climate consensus in China: "The environment - including climate - is the area with the biggest consensus view in [China]. It could be a test run for having more multi-stakeholder governance in our country."

The transcript below has been edited for length and clarity.

Carbon Brief: You have been at the forefront of environmental issues in China for decades. How would you describe the changes in China's approach to climate and environment issues over the time you've been observing them?

Ma Jun: I started paying attention to the issues when I got the chance to travel in different parts of China. I was struck by the environmental damage, particularly on the waterways, the rivers and lakes, which do not just have all these eco-impacts, but also expose hundreds of millions to health hazards.

That got me to start paying attention. So I authored a book called China's Water Crisis and readers kept coming back to me to push for solutions. I delved deeper into the research and I realised that it's quite complicated - not just that the magnitude [of the problem] is so big, but that the whole issue is quite complicated, because we copied rules, laws and regulations from the west but enforcement remained weak.

There are huge externalities, but companies would rather just cut corners to be more competitive, put simply. Behind that, there was a doctrine before of development at whatever cost. That was the starting point in China - not just for policymakers, even people in the street, if you asked them at that time, most likely [they] would say: "China's still poor. Let's develop before we even think about the environment."

But that started changing, gradually. Unfortunately, it needed the "airpocalypse" in Beijing and the big surrounding regions to really motivate that change.

In 2011, Beijing suffered from very bad smog and millions upon millions of people made their voices heard - that they want clean air.

The government lent an ear to them and decided to start from transparency, monitoring and disclosing data to the public. So two years after it started and people were being given hourly air quality data [in 2011] - you realised how bad it was. In the first month [of 2013], the monthly average was over 150 micrograms. The WHO standard was 10 at the time - now it's dropped to five. [Some news reports and studies, based on readings published at the time by the US embassy in Beijing, note significantly higher figures.]

We believe that it's good to have that data - of course, it's very helpful - but it's not enough. Keeping children indoors or putting on face masks are not real solutions, we need to address the sources. So we launched a total transparency initiative with 24 other NGOs calling for real-time disclosure of corporate monitoring data.

To our surprise, the ministry made it happen. From 2014, tens of thousands of the largest emitters, every hour, needed to give people air [quality] data, and every two hours for water [quality].

We then launched an app to help visualise that for neighbourhoods. For the first time, people could realise which [companies] are not in compliance. Even super-large factories - every hour, if they were not in compliance, then they would turn from blue to red [in the app].

And so many people made complaints and petitioned openly - sharing that on social media, tagging the official [company] account. That triggered a chain reaction and changed that dynamic that I described.

From that moment, it was no longer easy for mayors or [party] secretaries to try to interfere with the enforcement, because it's being made so transparent, so public. The [environmental protection] agencies got the backing from the people and knocked the door open - and pushed the companies to respond to the people.

Then, the data is also used to enable market-based solutions, such as green supply chains and green finance.

Starting first with major multinationals and then extending to local companies, companies compared their lists with our lists before they signed contracts. If any of their [supplier] companies were having problems, they could get a push notification to their inbox or cell [mobile] phone.

That motivates 36,000 [companies] to come to an NGO like us - to our platform - to make that disclosure about what went wrong and how we try to fix the problem, and after that measure and disclose more kinds of data, starting with local emission data and now extending to carbon data.

And for banking and green finance, an NGO like us now helps banks track the performance of three million corporations who want to borrow money from them, as part of the due diligence process. These are just tiny examples to try to demonstrate that there's a real change.

Before, when I got started, the level of transparency was so limited. When we first looked at government data, at the beginning, there were only 2,000 records of enforcement. So we launched an index, assessed performance for 10 years across 120 cities.

During this process, [we also saw] consensus being made. In 2015, China's amended Environmental Protection Law [came into effect] and created a special chapter - chapter five - titled [information] transparency and public participation. That was the first ever piece of legislation in China to have such a chapter on transparency.

CB: What motivated that? Was it because they'd already seen this big public backlash?

MJ: They started listening to people and the demand for change, for clean air. And then they started seeing how the data can be used - not to disrupt the society, but to help to mobilise people.

The ministry felt that they had the backing from the people, basically, which helped them to gain confidence that data can be helpful and can be used in a responsible way. Before, they were always concerned about the data, particularly on disruption of social stability, because our data is not that beautiful at the beginning, due to the very serious pollution problem.

When our organisation got started, nearly 20 years ago, 28% of the monitored waterways - nationally-monitored rivers - reported water that was good for no use. Basically, it is so polluted that it's not good for any use. [Some] 300 million [people] were exposed to that in the countryside, it was very serious.

We're talking about the government changing its mindset. Of course, the reality is that they found [the data] can be used the responsible way and can be helpful, so they decided to embrace that and to tolerate that, to gradually expand transparency.

Now, China is aligning its system with the International Sustainability Standards Board (ISSB). The environment ministry also created a disclosure scheme, with 90,000 of China's largest [greenhouse gas] emitters on the list. We and our NGO partners tried to help implement that. We're talking about billions of tonnes of carbon emissions.

It would have been hard to imagine before, but we're talking about what's probably the largest scale of corporate measuring and disclosure now happening [anywhere in the world].

Of course, it's still not enough. Last year, we also helped the agency affiliated with the ministry to develop a guideline on voluntary carbon disclosure, targeting small and medium sized companies. We now have a new template on our platform - powered by AI - and a digital accounting tool that helps our users measure and disclose nearly 70m tonnes [of carbon dioxide equivalent] last year.

CB: Is there appetite on the industrial side to proactively get involved? Or is local regulation needed that mandates involvement?

MJ: At the beginning, no. If we have the dynamic that I described - at the beginning, whoever cut corners became more competitive. This caused a "race to the bottom" situation and even good companies find it quite difficult to stick to the rules.

But then the dynamic changed. Whoever's not in compliance with the law will be kicked out of the game. Not only would they receive increasingly hefty penalties or fines, but the data will be put into use in supply chains. Many of our users - the brands - integrate that data into their sourcing, meaning that if [suppliers] don't solve the problem they will lose contracts. And also banks could give them an unfavourable rating.

All this joint effort could create some sort of - of course, it's [only a] chance - but some kind of a stick. But it's also a kind of carrot, because those who decided to do better now benefit. If someone loses business [because they cannot help their consumer with compliance], then that business will [instead] go to those who want to go green.

This change in dynamic is very helpful. It started from the pollution control side and now we want to see that happen on the climate side. That's why we decided to develop the blue map for zero carbon, to try to map out and further motivate the decarbonisation process - region by region, sector by sector.

You asked about corporations - this is extremely important. China is the factory of the world and 68% of carbon emissions still relate either to the direct manufacturing process or to energy consumption to power the industrial production. So it is very important to motivate them, to create both rules and stimulus - both stick and carrot.

But if you don't have a stick, you can never make the carrot big enough. That is an externality problem, you never really solve that. We've now managed to solve the basic problem - non-compliance and outrageous violations. But that's the first step. Deep decarbonisation - not just scope one and two, but extending further upstream to reach heavy industry, the hard-to-abate industries - now this is the challenge.

CB: What are your expectations for industrial decarbonisation more broadly, especially given the technology bottlenecks?

MJ: There are still bottlenecks, but we see, actually, some progress is being made. Now corporations in China understand that they need to go in [a low-carbon] direction and some of them are actually motivated to develop innovative solutions.

For example, several major steel manufacturers managed to be able to find ways to produce much lower-carbon steel products. In the aluminium [sector] they also tried and also batteries. Unfortunately, these remain as only pilot projects.

When we engage with them and ask why they didn't expand production, they say that producing these items will have a "green premium", but no one wants to pay for that. Their users only want to buy tiny volumes for their sustainability reports - for the rest, they just want the low-cost ones.

They said, the more we produce the green products, the bigger our losses. So we decided to leave these products in our warehouse.

Then we engaged with the brands - the real estate industry, the largest user of iron and steel - and the automobile industry, the second largest. They claimed that if they [purchase greener materials], they would pay a green premium, but their users and consumers have no idea about [green consumption]. They only want to buy the cheapest products - and the more [these manufacturers] produce, the more they suffer losses.

So this means we need a mechanism, with multi-stakeholder participation, to share the burden of that transition - to share that cost of the green transition.

That green premium can only be shared, not one single stakeholder can easily absorb all of this given all the breakneck competition in China - involution - it's very, very serious and so companies are all stuck there.

What we're trying to do is to help change that. We assessed the performance of 51 auto brands and tried to help all the stakeholders understand which ones could go low-carbon.

But it's not enough just to score and rank them. We also need to engage with the public, to have them start gaining an understanding that their choice matters. So how - it's more difficult, you know? Pollution is much easier. We told them: "Look, people are dumping all this waste."

CB: It's all visible.

MJ: Yeah, when people suffer so seriously from pollution - air, water and soil pollution - they feel strongly. They wrote letters to the brands, telling them that they like their products but they cannot accept this.

But on climate, it's more abstract - [we're talking about] the end of the century or the polar bears. People don't feel that it's linked with their own individual behaviour or consumption choices.

We decided to upgrade our green choice initiative to the 2.0 level. This new solution we developed is called product carbon scan. Basically, you take a picture of any product and services products and an AI [programme] will figure out what product that is and tell you the embodied carbon of that product.

Now, it's getting particularly sophisticated with automobiles. The AI now - from this year - for most of the vehicles on the streets of China, can figure out not just which brand it is, but which model. We have all these models in our database - 700-800 models and 7,000-8,000 varieties of cars, all of which have specific carbon footprints.

CB: How do you account for all of the different variables? If something changes upstream, if a supplier changes - how do you account for that?

MJ: The idea is like this - now, this is mostly measured by third parties, our partners. We also have our emission factors database that we developed. So we know that, as you said, there are all these variables. For the past six months, we got our users to take pictures of 100,000 cars. We distributed them to 50 brands and [calculated] that the total carbon footprint was 4.2m tonnes, for the lifecycle of these 100,000 cars. Each brand got their own share of this.

So we wrote letters - and we're still writing letters now, 10 NGOs in China, we're writing letters now to the CEOs of these 50 brands - to tell them that this is happening. Our users, consumers of their products, are paying attention to this and are raising questions. We have two demands.

First, have you done your own measuring for the product you sell in China? Do you have plans to measure and disclose those specific details? Because if third parties can do it, so can they. It's not space technology, they can do it and obviously they own all this data. They understand much better about the entire value chain and it's much easier for them to get more accurate figures. With the "internet of things" and new technologies, for some products, they can get those details already, so the auto industry should be getting close to [achieving] that.

The second question is, you all have set targets for carbon reduction and carbon neutrality. We know that most of you are not on track. Even the best ones - Mercedes-Benz is at the top of our rankings - are seeing their carbon intensity going up. Not just the total volume [of emissions], but products' carbon intensity is going up instead of going down. So, obviously, they haven't really decarbonised their upstream - steel and aluminium. So [we ask them]: "What's your plan? Can you give me an actionable, short- or mid-term plan on the decarbonisation of these upstream, hard-to-abate sectors?"

I think this is the way to try to tap into the success of pollution control and now extend that to cover carbon.

CB: It seems a challenge facing China's climate action that policymakers often flag is MRV [monitoring, reporting and verification] and data in general. You're the expert on this. Would you agree? Are there big challenges around MRV that China needs to address before it can progress further?

MJ: This is a prerequisite, in my view. To have [to] measure, disclose and allow access to data is a prerequisite for any meaningful multi-stakeholder effort. I wouldn't underestimate the challenge in the follow-up process - the solutions, the innovations, the new technologies that need to be developed to decarbonise - but it will be impossible to get started without proper, more comprehensive measuring and disclosure, and without having more credible data available.

I take this as a starting point - a most important starting point. I'm so happy to see that there's a growing consensus on that. In China, the government decided to embrace the concept of the ISSB, embrace the concept of ESG reporting, and to allow an NGO like us to try to help with the disclosure mechanism.

This is very powerful and very productive, and the reason that we could create that solution is because China pays so much attention to product carbon footprints, of course, motivated by the EU legislations, like the carbon border adjustment mechanism (CBAM) and others. In some ways, it's quite interesting to see the EU set these very progressive rules, but then China responds and decides to create solutions and scale them up.

On the product carbon footprint alone, the Ministry of Ecology and Environment (MEE) coordinated 15 different ministries to work on it, with a very tight schedule - targets set for 2027 and then 2030 - [implying] very fast progress. We work together with our partners on a new book telling businesses - based on emission factors - how to handle it and how to proceed, in terms of practical solutions.

All this is just to say that, on the data and MRV side, China has already overcome its initial reluctance, or even resistance. Now [it] is in the process of not just making progress and expanding data transparency, but also trying to align that with international practice.

And at COP30, I actually launched a new report [titled the Global City Green and Low-Carbon Transparency Index]…The transparency index actually highlighted that, of course, developed cities are still doing better, but a whole group of Chinese cities are quickly catching up. Trailing behind are other global south cities.

When China decides to do something, it isn't just individual businesses or even individual cities [that see action taken]. There will be more of a platform-based system - meaning there is an [underlying] national requirement, which can help to level the playing field, with regions or sectors possibly taking up stricter requirements, but not being able to compromise the national ones [by setting lower targets].

So, with MRV, I have some confidence. That doesn't mean it's easy. Particularly on the product carbon footprint, there are so many challenges. Trying to make emission factors more accurate is quite difficult, because products have so many components and the whole value chain can be very long and complicated. But with determination, with consensus, I'm still confident that China can deliver.

And in the meantime, what is now going on in China, increasingly, could become a contribution to global MRV practice.

CB: It's interesting that you mentioned that. Talking to people at the COP30 China pavilion, people from global south countries see China as a climate leader and want to learn about what's going on in China. By contrast, developed countries seem more focused on the level of ambition in China's NDC [its climate pledge, known as a nationally determined contribution]. How would you view China's role in climate action in the next five years?

MJ: On the NDC, my personal observation - I come from an NGO, so I don't represent the government's decision here - is that culturally, there's some sort of differences, nuanced differences - or very obvious differences - here.

In the west, the cultural tendency is that if you want to show that you're serious, you need to set an ambitious target. Even if, at the end of the day, you fail, it doesn't mean that you're bad, you still achieve more than if you'd set a lower target. That's the mentality.

But in China, the culture is that it is embarrassing if you set a target and you fail to fully honour that commitment. So they tend to set targets in a slightly more conservative way.

I'm glad to see that [China's] NDC is leaving space for flexibility - it said that China will try to achieve a higher target. This is the tone, and in my view it gives us the space and the legitimacy to try to motivate change and develop solutions to bend the curve faster. Even if the target is not that high, we know that we will try to beat that.

And then, there's the renewables target for 1,200 gigawatts (GW) by 2030, a target that was achieved last year - six years early. Now we've set a target of 3,600GW - that means adding 180GW every year. But, as you know, over the past several years [China's renewable additions] have been above 200GW.

So you can see that there's a real opportunity there and we know that China will try to overdeliver. There's no kind of a good or bad, or right or wrong, with these two different cultural [approaches].

But one thing I hope that we all focus more on is implementation - on action. Because we do see that, for some of the global targets that have already been set, no-one seems to be paying any real attention to them - such as the tripling of [global] renewable capacity.

We all witnessed that, in Dubai at COP28, a target was agreed and accepted by the international community. China's on track, but what about the others? Most countries are not on track.

The global south, it's not only for their climate targets - the [energy] transition is essential for their SDG [sustainable development goal] targets. But now they lag so far behind. That's a pity, because now there's enough capacity - and even bigger potential - to help them access all this much faster.

But geopolitical divides, resource competition, nationalism, protectionism - all of this is dividing us. It's making global climate governance a lot more difficult and delaying the process to help [others in the] global transition. It's very difficult to overcome these problems - probably it will get worse before it gets better.

But if we truly believe that climate change is an existential threat to our home planet, then we should try to find a way to collaborate a bit more. The starting point could be transparency - that could be one of the ways to help bridge the gap.

In China, we used to have a massive gap of distrust between different stakeholders. People hated polluting factories, but they also had suspicions around government agencies giving protection to those factories. So there's all this distrust.

With transparency, it's easier for trust to be built, gradually, and the government started gaining confidence [in sharing data] because they saw with their own eyes that people came together behind them. Before, [people] always suspected that [the government] were sheltering the polluters. But from that moment, they realised that the government was serious and so gave them a lot of support.

Globally - maybe I'm too negative - I do think that it would [improve the chances for us all to collaborate] if we had a global data infrastructure and a global data platform, that doesn't just give [each country's] national data but drills down - province by province, city by city, sector by sector and, eventually, to individual factories, facilities and mines. For each one of these, there would be a standardised reporting system, giving people the right to know. I think through this we could build trust and use it as a starting point for collaboration.

I sit on several international committees - on air, water, the Taskforce on Nature-related Financial Disclosures (TFND), transition minerals, and so on. In each of these, I often make suggestions on building global data infrastructure. Increasingly, I see more nodding heads, and some have started to make serious efforts. TNFD is one example. They already have a proposal to develop a global data facility on data. The International Chamber of Commerce also put forward a proposal on the global data infrastructure on minerals and other commodities.

Of course, in reality, there will be many difficulties - data security, for example. So maybe it cannot be totally centralised, we need to allow for decentralised regional systems, but you could also create catalogues to allow the users to [dig into] all this data.

CB: And that then inspires people to look into issues they care about?

MJ: Yes and through that process, we will create more consensus, create more trust and gradually formulate unified rules and standards.

And we need innovative solutions. In today's world, security is something that's not just paid attention to by China, in the west it's a similar [story]. There are a lot of concerns about data security - growing concerns - so I think eventually there will be innovation to solve them. I'm still hopeful!

CB: Speaking of international cooperation, how has the withdrawal of the US from the Paris Agreement affected prospects for China-EU cooperation?

MJ: It will have a mixed impact, of course. Having the largest economy and second-largest emitter withdraw will have a big impact on global climate governance, and will in some way create negative pressure on other regions, because we're all facing the question of: "If they don't do it, why should we?" We also have those questions back home. I'm sure the EU is also facing this question.

But in the meantime, I hope that China and the EU realise that they have no choice but to work together - if they still, as they claim, truly believe in [the importance of] recognising the existential threat posed by climate change, then what choice do they have but to work together?

Fundamentally, we need a multilateral process to deal with this global challenge. The Paris Agreement, with all its challenges, still managed to help us avoid the worst of the worst. We still need this UNFCCC process and we need China and the EU to help maintain it.

At the last COP[29 in Azerbaijan], for the first time, it was not China and the US who saved the day. Before, it was always the US and China that made a deal and helped [shepherd] a global agreement. But last year, it was China and the EU that made the agreement and then helped to reach [a global deal] in Azerbaijan.

I do think that China and the EU have both the intention and the innovative capacity, as well as a very, very powerful business sector. I'm still hopeful that these two can come together at this COP [in Brazil].

CB: We've spoken a lot about heavy industry and industrial processes. Coal is a very big part of China's emissions profile. In the short term, how do you see China's coal use developing over the next five to 10 years?

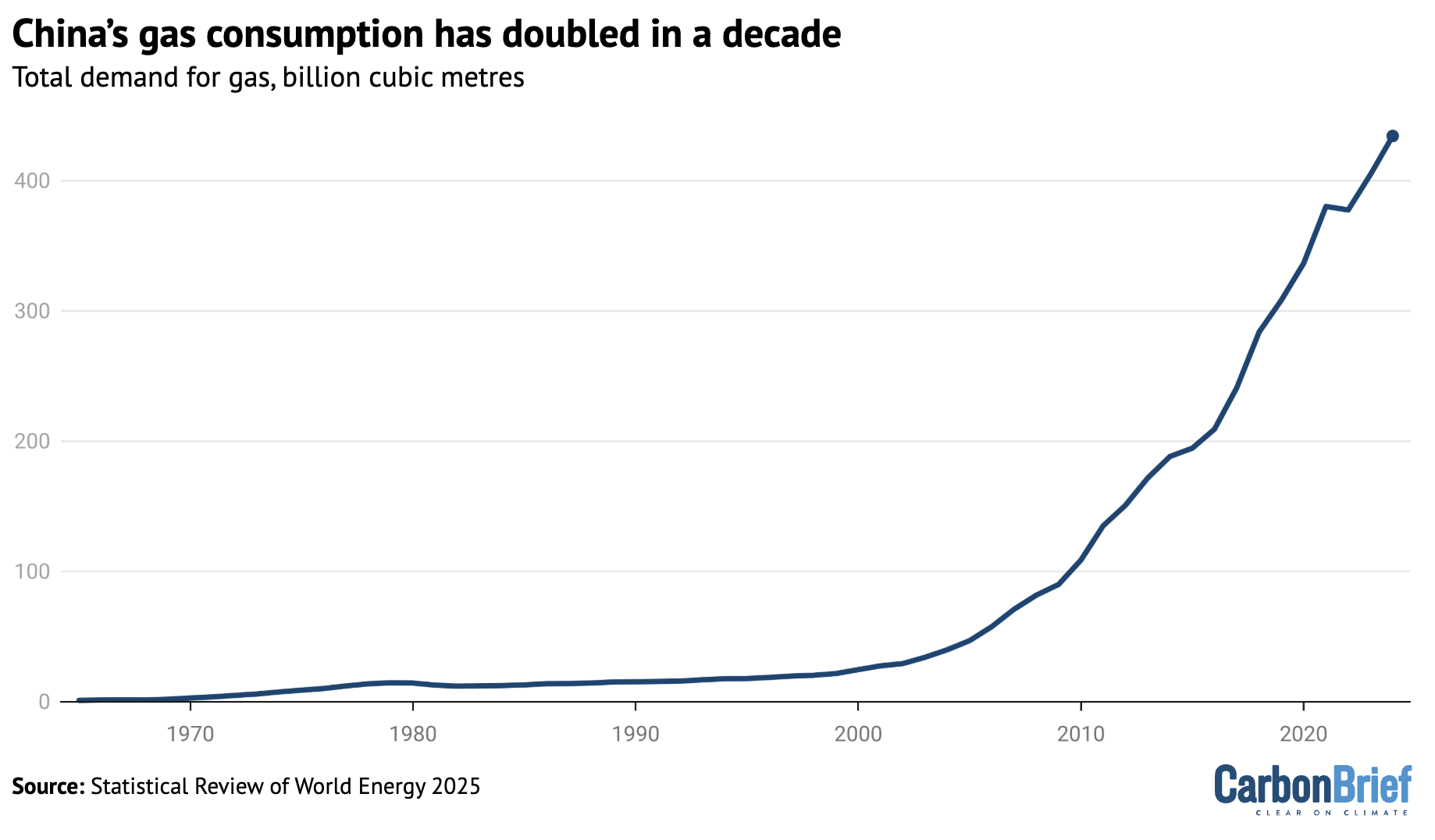

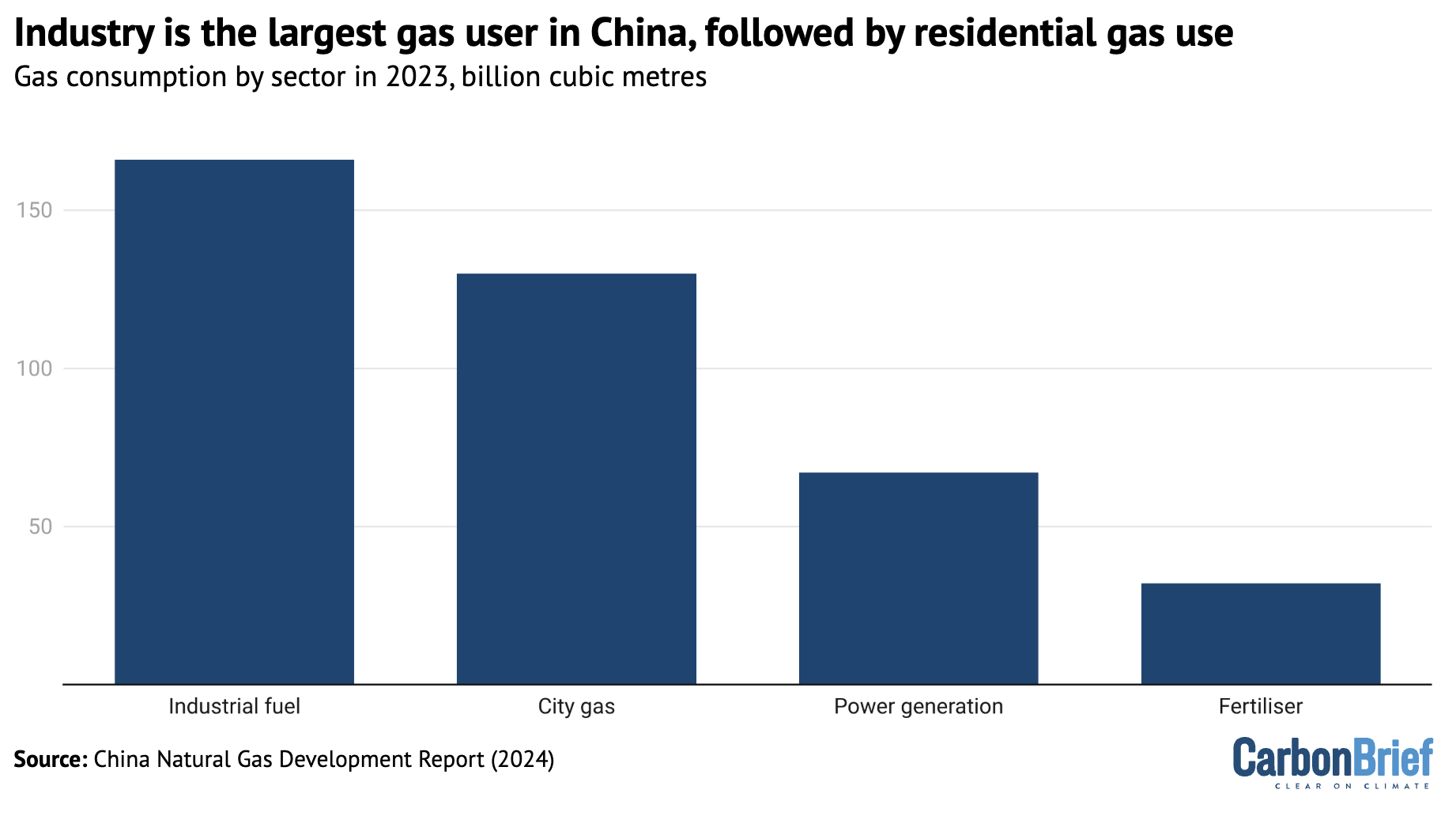

This ties into that complicated issue of the geopolitical divide. The original plan was to use natural gas as the transition [fuel], which would make things much easier. But geopolitical tensions means gas is no longer considered safe and secure, because China has very little of this resource and has to depend on the other regions, including the US, for gas.

That, in some way, pushed towards authorising new coal power plants and, in some way, we are all suffering for that. In the west as well. We all have to create massive redundancies for so-called insecurity, we're all bearing higher costs and we're all facing the risk of stranded assets, because we have such a young coal-power fleet.

The only thing we can do is to try to make sure that these plants increasingly serve only as a backup and as a way to help absorb high penetration of renewables, because now this is a new challenge. Renewables have been expanding so fast that it's very difficult - because of its intermittent nature - to integrate it into the power grid. New coal power can help absorb, but only if we can make [it] a backup and not use it unless there's a need. Of course, that means we have to pay to cover the cost for those coal plants.

The funny thing is that there's no business interest for the coal sector to carry on, because increasingly the market will trend towards using renewables, because it's getting cheaper and cheaper. So the coal sector, for security and integration of renewables, will be kept. But it will play an increasingly smaller role. In the meantime, the coal sector can help balance the impact through making chemicals, rather than just energy.

In the meantime, [we need to] try to find ways to accelerate the whole energy transition and electrify our economy even faster. That's a clear path towards both carbon peaking and carbon neutrality in China.

It's already going on. Carbon Brief's research already highlights some of the key issues, such as from March [2024] emissions are actually going down. That cannot happen without renewables, because our electricity demand is still going up significantly. In the meantime, the cost of electricity is declining.

This allows China to find its own logic to stick to the Paris Agreement, to stick to climate targets and even try to expand its climate action, because it can benefit the economy. It can benefit the people.

I think Europe probably could also learn from that, because Europe used to focus on climate for the climate's sake. With [the Russia-Ukraine] war going on, that makes it even more difficult.

CB: You mean the green economy narrative?

MJ: Yes, the green economy narrative is not highlighted enough in Europe. Now, suddenly, it's about affordability, it's about competition, and suddenly they feel that they're not in a very good position. But China actually focuses more on the green economy side. China and the EU could - hand-in-hand - try to pursue that.

CB: That leads perfectly to my last question. How important is the role of civil society now in developing climate and environmental policy in China?

MJ: We all trust in the importance of civil society. This is our logo, which we designed 20 years ago. Here are three segments: the government, business and civil society.

IPE director Ma Jun showing a pin based on his organisation's logo. Photo credit: Carbon Brief

IPE director Ma Jun showing a pin based on his organisation's logo. Photo credit: Carbon Brief

Civil society should be part of that. But we all, realistically, understand that the government is very powerful, businesses have all the resources, but civil society is still very limited in terms of its capacity to influence things.

But still, I'm glad to see that we have a civil society and NGOs like us continue to have the space in China to do what we're doing. What we're doing is based on these principles of transparency, the right to know. It's based on the participation of the public. It's based on the rule of law. We cherish that and we still have the space to work [on these issues].

We're lucky, because the environment - including climate - is the area with the biggest consensus view in our society. It could be a test run for having more multi-stakeholder governance in our country. I hope that, increasingly, this can help build social trust between stakeholders and to see [climate action] benefit society in this way.

I know it's not easy - there are still a lot of challenges [for NGOs] and not just in China. We work with partners in other regions - south-east Asia, south Asia, Africa and Latin America - and it's hard to imagine the challenges they could face, such as serious challenges to their personal safety.

Now, even in the global north, NGOs are under pressure. So we have a common challenge. Back to the issue of transparency. I hope that transparency also can be a source of protection for NGOs.

When all of us need to [take action to address climate issues], whether that be taking samples of water, protesting on the ground - being face-to-face and on the front line - without some sort of multi-stakeholder governance, then it will be far more difficult for NGOs to participate.

If the government can provide environmental monitoring data to the public, if corporations can make self-disclosures, then it will help with this, to some extent. Because it's not new - environmental blacklists in China are managed by the government, based on data, based on a legal framework. That can be a source of protection.

So I hope that NGO partners in other parts of the world can recognise that we should work together to promote transparency.

CB: Thank you.

Analysis: China's CO2 emissions have now been 'flat or falling' for 21 months

China energy

|12.02.26

China energy

|05.02.26

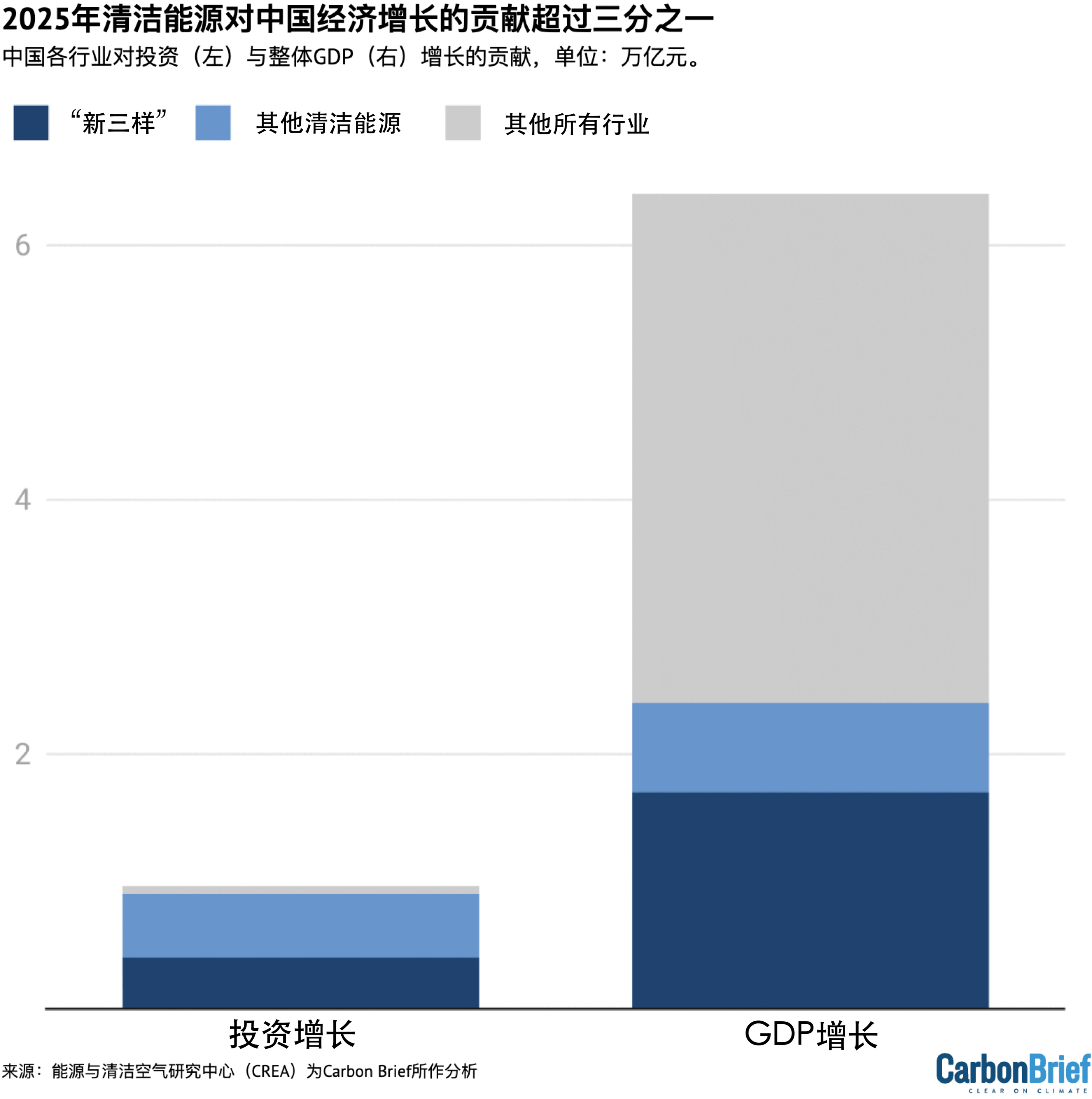

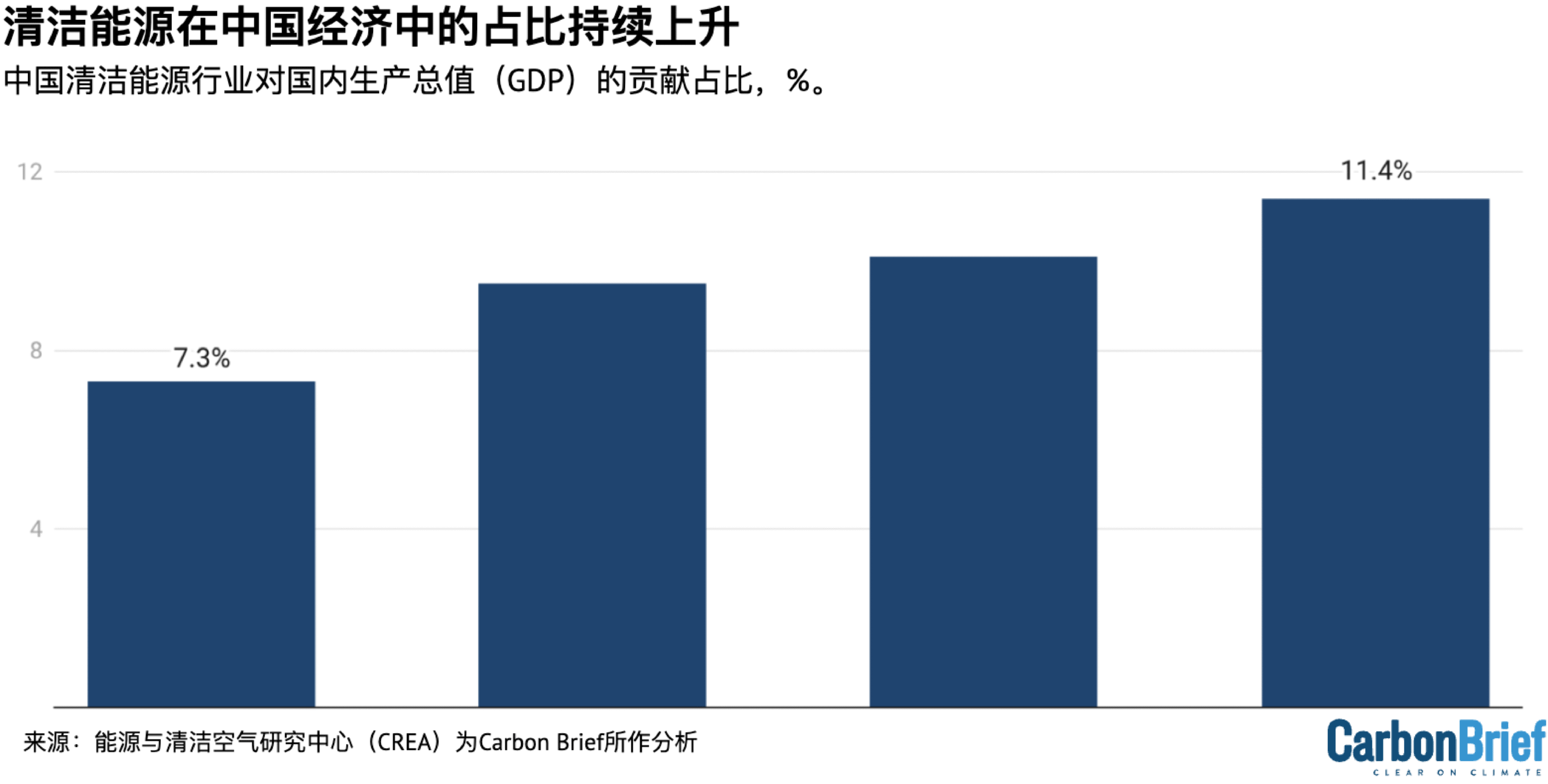

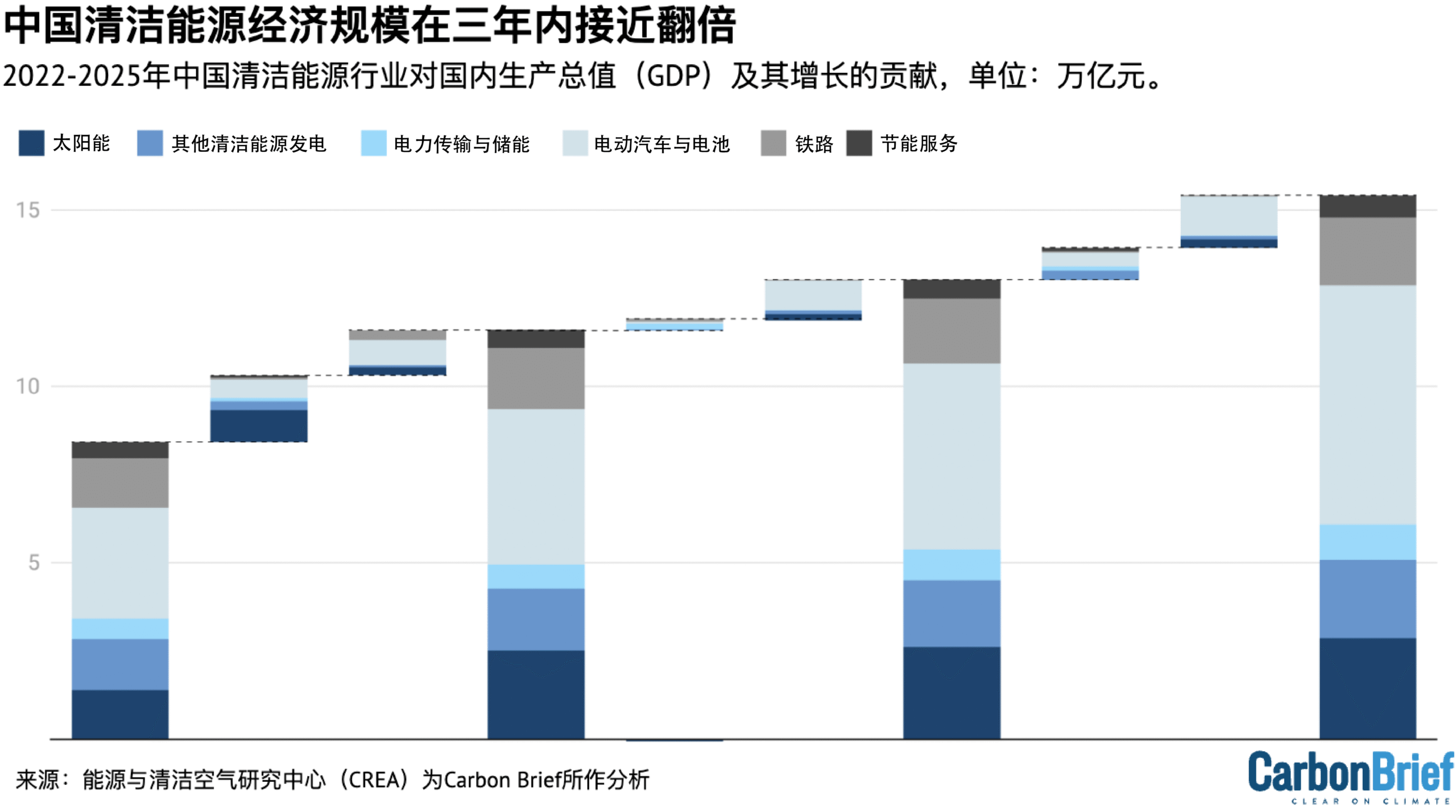

Analysis: Clean energy drove more than a third of China's GDP growth in 2025

China energy

|05.02.26

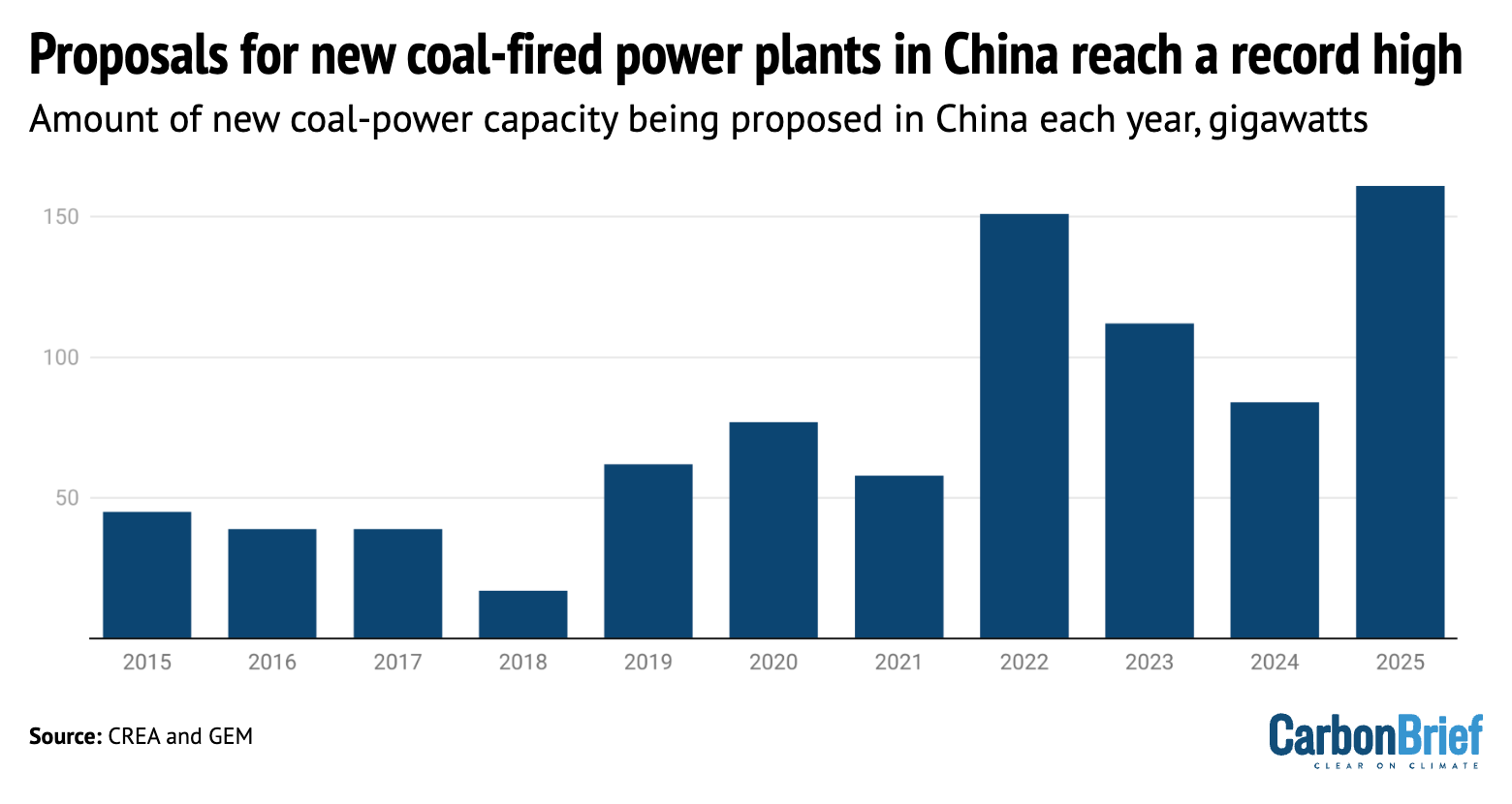

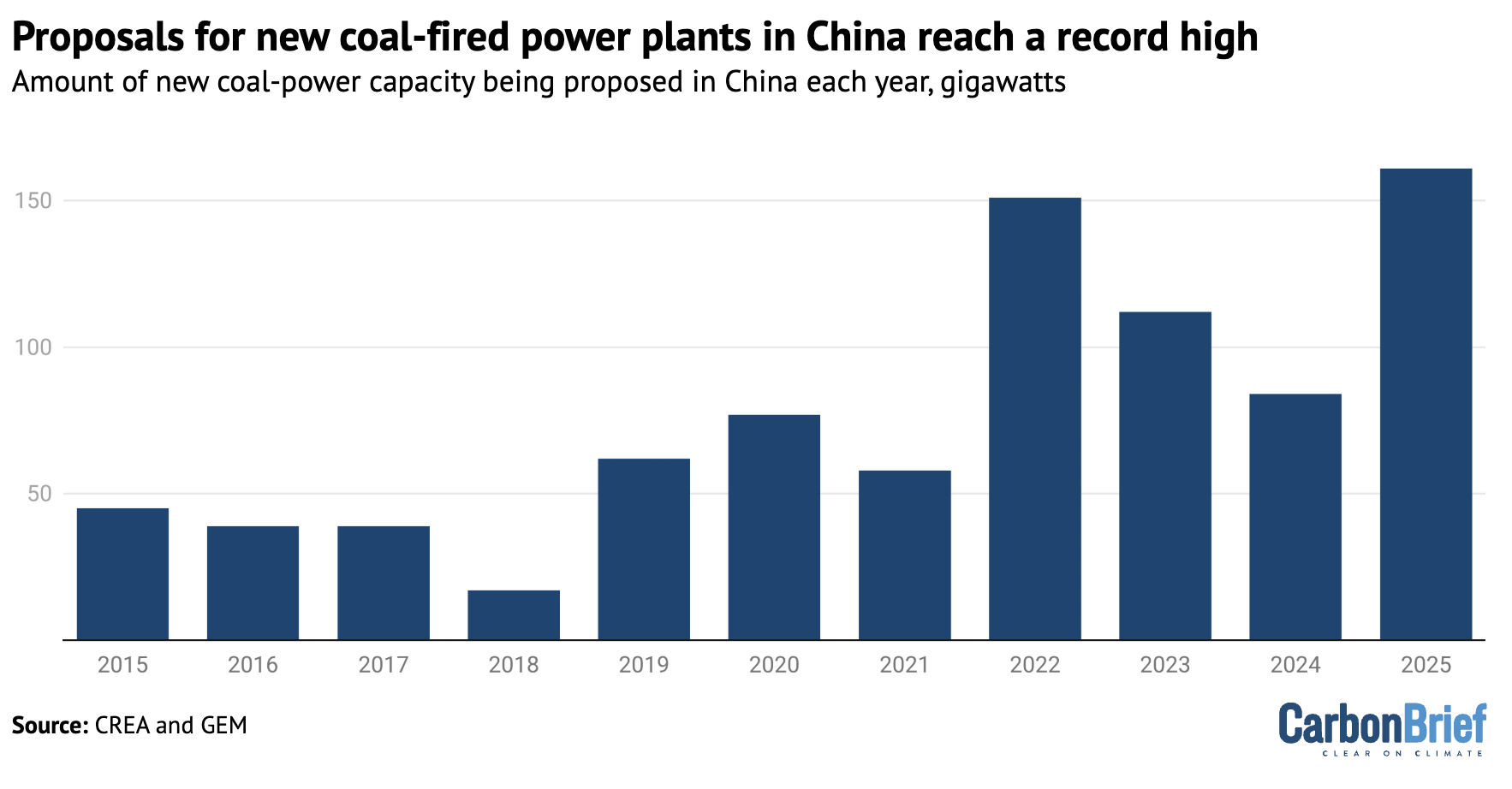

'Rush' for new coal in China hits record high in 2025 as climate deadline looms

China energy

|03.02.26

jQuery(document).ready(function() { jQuery('.block-related-articles-slider-block_1f4447154486567cb00c7f41b8c9e11b .mh').matchHeight({ byRow: false }); });The post Ma Jun: 'No business interest' in Chinese coal power due to cheaper renewables appeared first on Carbon Brief.

The economics of clean energy "just get better and better", leaving opponents of the transition looking like "King Canute", says Chris Stark.

Stark is head of the UK government's "mission" to deliver clean power by 2030, having previously been chief executive of the advisory Climate Change Committee (CCC).

In a wide-ranging interview with Carbon Brief, Stark makes the case for the "radical" clean-power mission, which he says will act as "huge insurance" against future gas-price spikes.

He pushes back on "super daft" calls to abandon the 2030 target, saying he has a "huge disagreement" on this with critics, such as the Tony Blair Institute.

Stark also takes issue with "completely…crazy" attacks on the UK's Climate Change Act, warns of the "great risk" of Conservative proposals to scrap carbon pricing and stresses - in the face of threats from the climate-sceptic Reform party - the importance of being a country that respects legal contracts.

He says: "The problems and woes of this country, in terms of the cost of energy, are due to fossil fuels, not due to the Climate Change Act."

The UK should become an "electrostate" built on clean-energy technologies, says Stark, but it needs a "cute" strategy on domestic supply chains and will have to interact with China.

Beyond the UK, despite media misinformation and the US turn against climate action, Stark concludes that the global energy transition is "heading in one direction":

"You've got to see the movie, not the scene. The movie is that things are heading in one direction, towards something cleaner. Good luck if you think you can avoid that."

- On the rationale for clean power 2030: "We're trying to do something radical in a short space of time…It has all the characteristics of something that you can do quickly, but which has long-term benefit."

- On grid investment: "[T]he programme of investment in infrastructure and in networks is genuinely once in a generation and we haven't really done investment at this scale since the coal-fired generation was first planned."

- On 88 "critical" grid upgrades: "We really need them to be on time, because the consumer will see the benefit of each one of those upgrades."

- On electricity demand: "I think we are in the point now where we are starting to see the signal of that demand increase - and it is largely being driven by electric vehicle uptake."

- On high electricity prices: "[I]t's largely the product of decades of [decisions] before us. We do have high electricity prices and we absolutely need to bring them down."

- On industrial power prices: "[W]e've got a whole package of things that…[will] take those energy prices down very significantly, probably below the sort of prices that you'll see on the continent."

- On cutting bills further: "The investments that we think we need for 2030…will add to some of those fixed costs, but…facilitate a lower wholesale price for electricity, [which] we think will at least match and probably outweigh those extra costs."

- On insuring against the next gas price spike: "The amount of gas we're displacing when that [new renewable capacity] comes online is a huge insurance [policy] against the next price spike that [there] will be, inevitably, [at] some point in the future for gas prices."

- On Centrica boss Chris O'Shea's comments on electricity bills in 2030: "I don't think he's right on this…I'm much more optimistic than Chris is about how quickly we can bring bills down."

- On the need for investment: "I think there's a hard truth to this, that any government - of any colour - would face the same challenge. You cannot have a system without that investment, unless you are dicing with a future where you're not able to meet that future demand."

- On the high price of gas power: "If you don't think that offshore wind is the answer for [rising electricity demand], then you need to look to gas - and new gas is far more expensive."

- On calls to scrap the 2030 mission: "I have a huge disagreement with the Tony Blair Institute on this…I think it's daft - like, super daft - to step back from something that's so clearly working."

- On Conservative calls to scrap carbon pricing: "We absolutely have to have carbon pricing…if you want to make progress on our climate objectives. It also has been a very successful tool…I think it's a great risk to start playing around with that system."

- On gas prices being volatile: "[A]t the time that Russia invaded Ukraine…the global gas price spiked to an extraordinary degree…I'm afraid that is a pattern that is repeated consistently."

- On insulating against gas price spikes: "[Y]ou cannot steer geopolitics from here in the UK. What you can do is insulate yourself from it…Clean power is largely about ensuring that."

- On Reform threats to renewable contracts: "[A]ll this sort of threatening stuff, that is about ripping up existing contracts, has a much bigger impact than just the energy transition. This has always been a country that respects those legacy contracts."

- On the wider benefits of the clean-power mission: "In the end, we're bringing all sorts of benefits to the country that go beyond the climate here. The jobs that go with that transition, investment that comes with that and, of course, the energy security that we're buying ourselves by having all of this domestic supply. It's hard to argue that that is bad for the country."

- On the UK's plans for a renewable-led energy system: "[The] idea of a renewables-led system, with nuclear on the horizon, is just so clearly the obvious thing to do. I don't really know what the alternative would be for us if we weren't pursuing it."

- On the UK becoming an "electrostate": "Yes, that's quite good for the climate…It's also extraordinarily good for productivity, because you're not wasting energy. Fossil fuels bring a huge amount of waste…You don't get that with electrotech. I want us to be an electrostate."

- On bringing supply chains and Chinese technology: "I want to see us adopt electrotech. I also want us to own a large part of the supply chain…I don't think it's ever going to be the case that we can…avoid the Chinese interaction…[B]ut I think it's really important that our industrial strategy is cute about which bits of that supply chain it wants to see here."

- On attacks on UK climate policy: "A lot of the criticism of the Climate Change Act I find completely…crazy. It has not acted as a straitjacket. It has not restricted economic growth. The problems and woes of this country, in terms of the cost of energy, are due to fossil fuels, not due to the Climate Change Act."

- On media misinformation: "[C]limate change and probably net-zero have taken on a role in the 'culture wars' that they didn't previously have."

- On winning the argument for clean power: "Actually, it's not to shoot down every assertion that you know to be false. It's just to get on with trying to do this thing, to demonstrate to people that there's a better way to go about this."

- On net-zero: "I think we are getting beyond a period where net-zero has a slogan value. I think it's probably moved back to being what it always should have been, really, which is a scientific target - and in this country, a statutory target that guides activity."

- On the geopolitics of climate action: "[I]t's striking how much it's shifted, not least because of the US…It is slightly weird…that has happened at a time when every day, almost, the evidence is there that the cleaner alternative is the way that the world is heading."

- On US withdrawal from the Paris Agreement: "I wish that hadn't happened, but the economics of the cleaner alternative that we're building just get better and better over time."

- On watching "the movie, not the scene": "The movie is that things are heading in one direction, towards something cleaner. Good luck if you think you can avoid that - [like] King Canute."

Carbon Brief: Thanks very much for joining us today. Chris, you're in charge of the government's mission for clean power by 2030. Can you just explain what the point of that mission is?

Chris Stark: Well, we're trying to do something radical in a short space of time. And maybe if I start with the backstory to that, Ed Miliband, as secretary of state, was looking for a project where he could make a difference quickly. And the reason that we are focused on clean power 2030 is because it is that project. It has all the characteristics of something that you can do quickly, but which has long-term benefits.

What we're trying to do is to accelerate a process that was already underway of decarbonising the power system, but to do so in a time when we feel it's essential that we start that journey and move it more quickly, because in the 2030s we're expecting the demand for electricity to grow. So this is a bit of a sprint to get ourselves prepped for where we think we need to be from 2030 onwards. And it's also, coming to my role, it's the job I want to do, because I spent many years advising that you should decarbonise the economy by electrifying - and stage one of that is to finish the job on cleaning up the supply.

So it's kind of the perfect project, really. And if you want to do clean power by 2030, [the] first thing is to say we're not going to take an overly purist approach to that. So we admit and are conscious - in fact, find it useful - to have gas in the mix between now and 2030. The challenge is to run it down to, if we can, 5% of the total mix in 2030 and to grow the clean stuff alongside it. So, using gas as a flexible source, and that, we think is a great platform to grow the demand for electricity on the journey, but especially after 2030 - and that's when the decarbonisation really kicks in.

So it's a sort of exciting thing to try and do. And if you want to do it, here comes the interesting thing. You need the whole system, all the policies, all the institutions, all the interactions with the private sector, interactions with the consumer, to be lined up in the right way.

So clean power by 2030 is also the best expression of how quickly we want the planning system to work, how much harder we want the energy institutions like NESO [the National Energy System Operator] and energy regulator Ofgem to support it - and how we want to send a message to investors that they should come here to do their investment. Turns out, it's a great way of advertising all of that and making it happen. And so far, it's working great.

CB: Thanks. So do you still think it's achievable? We're sitting in "mission control". You've got some big screens on the wall. Is there anything on those screens that's flashing red at the moment?

CS: So, right behind you are the big screens. And it's tremendously useful to have a room, a physical space, where we can plan this stuff and coordinate this stuff. There's lots of things that flash red. There's no question. And it's an expression of it being a genuine mission. This is not business as usual. So you wouldn't move as quickly as this, unless you've set your North Star around it. And it does frame all the things that, especially this department is doing, but also the rest of government, in terms of the story of where we are.

We're approaching two years into this mission and - really important to say - if the mission is about constructing infrastructure, it's in that timeframe that you'll do most of the work, setting it up so that we get the things that we think we need for 2030 constructed.

We're already reaching the end of that phase one, and we did that by first of all, going as hard and as fast as we could to establish a plan for 2030, which involved us going first to the energy system operator, NESO, to give us their independent advice. We then turned that into a plan, and the expression of that plan is largely that we need to see construction of new networks, new generation, new storage and a new set of retail models to make all of that stick together well for the consumer.

Phase one was about using that plan to try and go hard at a set of super-ambitious technology ranges for all the clean technologies, so onshore wind, offshore wind, solar [and] also the energy storage technologies. We've set a range that we're trying to hit by 2030 that is right at the top end of what we think is possible. Then we went about constructing the policies to make that happen.

Behind you on the big screens, what we're often doing is looking at the project pipeline that would deliver that [ambition]. At the heart of it is the idea that if you want to do something quickly by 2030, there is a project pipeline already in development that will deliver that for you, if you can curate it and reorder it to deliver. And therefore, the most important and radical thing that we did - alongside all the reforms to things like contracts for difference and the kind of classic policy support - is this very radical reordering of the connection queue, which allows us to put to the front of the queue the projects that we think will deliver what we need for 2030 - and into the 2030s.

Then, alongside that, the other big thing, and I think this is going to be more of a priority in the second phase of work for us, is the networks themselves. We are trying to essentially build the plane while it flies by contracting the generation whilst also building the networks, and of course, doing this connection queue reform at the same time. That is, again, radical, but the programme of investment in infrastructure and in networks is genuinely once in a generation and we haven't really done investment at this scale since the coal-fired generation was first planned. We think a lot about 88 - we think - really critical transmission upgrades. We really need them to be on time, because the consumer will see the benefit of each one of those upgrades.

CB: You already talked about electricity demand growing as the economy electrifies. Do you think that there's a risk that we could hit the clean power 2030 target, but at the same time, perhaps meeting it accidentally, by not electrifying as quickly as we think - and therefore demand not growing as quickly?

CS: So, an unspoken - we need to clearly make this more of a factor - an unspoken factor in the shape of the energy system we have today has been an assumption, for well over 20 years, really, that demand for electricity was always going to pick up. In fact, what we've seen is the opposite. So for about a quarter of a century, demand has fallen. Interestingly, the system - the energy system, the electricity system - generally plans for an increase in demand that never arrives. We could have a much longer conversation about why that happened and the institutional framework that led to that. But it is nonetheless the case.

I think we are at the point now where we are starting to see the signal of that demand increase - and it is largely being driven by electric vehicle uptake. The story of net-zero and decarbonisation does rest on electrification at a much bigger scale than just electric cars. So part of what we're trying to do is prepare for that moment.

But you're absolutely right, if demand doesn't increase, the biggest single challenge will be that we've got a lot of new fixed costs and a bigger system - on the generation side and the network side - that are being spread over a demand base that's too small. So, slightly counter-intuitively, because there's a lot of coverage around the world about the concern about the increase in electricity demand, I want that increase in electricity demand, but I also want it to be of a particular type. So if we can, we want to grow the demand for electricity with flexible demand, as much as possible, that is matching - as best we can - the availability of the supply when the wind blows or the sun shines. That makes the system itself cheaper.

The more electricity demand we see, the more those fixed costs that are in the system - for networks and increasingly for the large renewable projects - the more they are spread over a bigger demand base and the lower the unit costs of electricity, which will be good, in turn, for the uptake of more and more electrification in the future. So there's this virtuous circle that comes from getting this right. In terms of where we go next with clean power 2030, a big part of that story needs to be electrification. We want to see more electricity demand, again, of the right sort, if we can. More flexible demand and, again, [the] more that that is on the system, the better the system will operate - and the cheaper it will be for the consumer.

CB: So, the UK has among the highest electricity prices of any major economy. Can you just talk through why you think that is - and what we should be doing about it?

CS: Yeah, there's a story that the Financial Times runs every three months about the cost of electricity - and particularly industrial electricity prices. Every time that happens, we slightly wince here, because it's largely the product of decades of [decisions] before us.